425: Prospectuses and communications, business combinations

Published on January 12, 2026

Filed by Presidio PubCo Inc.

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Presidio PubCo Inc.

Commission File No.: 333-290090

Date: January 12, 2026

The following is an investor presentation relating to the proposed business combination with EQV Ventures Acquisition Corp., provided by Presidio Investment Holdings, LLC on January 12, 2026.

INVESTOR PRESENTATION

LEGAL DISCLAIMER 2 This presentation and any oral statements made in connection therewith have been prepared and are being provided on a confidential basis to assist interested parties in making their own evaluation with respect to the proposed Business Combination among EQV Ventures Acquisition Corp . (“EQV"), Presidio Investment Holdings LLC (“Presidio”), Presidio PubCo Inc . (“PubCo”) and certain other parties thereto, the acquisition by PubCo of EQV Resources LLC ("EQVR") and related transactions (the “Business Combination”), solely for discussion with those persons to whom it is transmitted and for no other purposes . This presentation and its contents contain proprietary information and may not be reproduced or disseminated, in whole or in part . No offering of securities is being made at this time . You should not rely on any of the information contained in this presentation in making any investment decision . Any such offering of securities will only be made by means of the registration statement on Form S - 4 (including a prospectus) filed with the Securities and Exchange Commission (“SEC”) by PubCo, Presidio and EQVR (as amended, the “Registration Statement”), after such registration statement becomes effective, or in a transaction exempt from such requirements . No such registration statement has become effective and no such exempted transaction has occurred as of the date of this presentation . The distribution of this presentation may also be restricted by law and persons into whose possession this presentation comes should inform themselves about and observe any such restrictions . The recipient acknowledges that (a) it is aware that the United States securities laws prohibit any person who has material non - public information concerning a company from purchasing or selling securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities, (b) it is familiar with the Securities Exchange Act of 1934 , as amended, and the rules and regulations promulgated thereunder (collectively, the "Exchange Act"), and (c) it will neither use, nor cause any third party to use, this presentation or any information contained herein in contravention of the Exchange Act, including Rule 10 b - 5 thereunder . Not an Offer This presentation and any oral statements made in connection therewith do not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of any securities in any state or jurisdiction, domestic or foreign, in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction . Such an offer or solicitation can only be made by way of an effective registration statement or applicable exemption from registration in accordance with the securities laws . The consummation of the proposed Business Combination is subject to various risks and contingencies, including customary closing conditions . There can be no assurance that the proposed Business Combination will be consummated as described herein or otherwise . Forward - Looking Statements Some of the statements contained in or made in connection with this presentation constitute “forward - looking statements” . Forward - looking statements relate to, but are not limited to, expectations, hopes, beliefs, intentions, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts . Terms such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” "will," “would” and similar expressions may identify forward - looking statements, but the absence of these words does not mean that a statement is not forward - looking . Actual events or results may differ materially from those discussed in forward - looking statements as a result of various risks and uncertainties, many of which are beyond our control . Many factors could cause actual future events to differ materially from these forward - looking statements, including but not limited to : changes in business, market, financial, political and legal conditions ; benefits from hedges and expected production ; the inability of the parties to successfully or timely consummate the proposed Business Combination, including the risk that any regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect PubCo or the expected benefits of the proposed Business Combination or that the approval of the shareholders of EQV is not obtained ; failure to realize the anticipated benefits of the proposed Business Combination, which may be affected by, among other things, competition, the ability of PubCo to grow and manage growth profitably, maintain key relationships and retain its management and key employees ; risks related to the uncertainty of the projected financial information ; risks related to Presidio’s current growth strategy ; the occurrence of any event, change or other circumstances that could give rise to the termination of any definitive agreements with respect to the proposed Business Combination ; the outcome of any legal proceedings that may be instituted against any of the parties to the potential Business Combination following its announcement and any definitive agreements with respect thereto ; changes to the proposed structure of the proposed Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the proposed Business Combination ; risks that Presidio or PubCo may not achieve their expectations ; the ability to meet stock exchange listing standards following the proposed Business Combination ; the risk that the proposed Business Combination disrupts the current plans and operations of Presidio ; costs related to the potential Business Combination ; changes in laws and regulations ; risks related to the domestication of EQV as a Delaware corporation ; risks related to PubCo’s ability to pay expected dividends ; the extent of participation in rollover agreements ; the amount of redemption requests made by EQV’s public equity holders ; and the ability of EQV or PubCo to issue equity or equity - linked securities or issue debt securities or enter into debt financing arrangements in connection with the proposed Business Combination or in the future ; and other risks and uncertainties set forth in the sections entitled “Cautionary Note Regarding Forward - Looking Statements” and “Risk Factors” in EQV’s final prospectus relating to its initial public offering dated August 6 , 2024 or in other documents filed by EQV with the SEC . If any of these risks materialize or EQV’s, Presidio’s, PubCo’s or EQVR’s assumptions prove incorrect, actual results could differ materially from the results expressed in, or implied by, these forward - looking statements . There may be additional risks that none of EQV, Presidio, PubCo nor EQVR presently knows or that each such party currently believes are immaterial that could also cause actual results to differ from those contained in the forward - looking statements . In addition, forward - looking statements reflect EQV’s, Presidio’s, PubCo’s and EQVR’s expectations, plans or forecasts of future events and views as of the date of this presentation . EQV, Presidio, PubCo and EQVR anticipate that subsequent events and developments will cause EQV’s, Presidio’s, PubCo’s and EQVR’s assessments to change . However, while EQV, Presidio, PubCo and EQVR may elect to update these forward - looking statements at some point in the future, EQV, Presidio, PubCo and EQVR specifically assume no obligation and do not currently intend to do so, whether as a result of new information, future events or otherwise, except as may be expressly required by applicable law . The information set forth herein does not purport to be complete, is unaudited and subject to change . These forward - looking statements should not be relied upon as representing EQV’s, Presidio’s, PubCo’s and EQVR’s assessments as of any date subsequent to the date of this presentation . None of EQV, Presidio, PubCo nor EQVR gives any assurance that Presidio, or the combined company (if the proposed Business Combination is consummated), will achieve its expectations . Accordingly, undue reliance should not be placed upon the forward - looking statements as predictions of future events, performance or achievements . Use of Industry and Market Data No representations or warranties, express or implied are given in, or in respect of, this presentation and any oral statements made in connection therewith . Industry and market data used in this presentation have been obtained from third - party industry publications and sources . None of EQV, Presidio, PubCo nor EQVR has independently verified the data obtained from these sources nor can assure you of the data’s accuracy or completeness . This data is subject to change . No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any projections or modeling or any other information contained herein . Any data on past performance or modeling contained herein is not an indication as to future performance . None of EQV, Presidio, PubCo nor EQVR assume any obligation to update the information in this presentation . This presentation also contains estimates and other statistical data made by independent parties and by Presidio relating to reserves, operations and growth and other data about Presidio’s industry . This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates . In addition, projections, assumptions and estimates of the future performance of Presidio and the combined company (if the proposed Business Combination is consummated) are necessarily subject to a high degree of uncertainty and risk . Additional Information and Where to Find It The Registration Statement includes a preliminary prospectus with respect to PubCo’s securities to be issued in connection with the proposed Business Combination and a preliminary proxy statement with respect to the shareholder meeting of EQV to vote on the proposed Business Combination . EQV, PubCo, Presidio and EQVR also plan to file other documents and relevant materials with the SEC regarding the proposed Business Combination . The Registration Statement has not yet been declared effective by the SEC . After the Registration Statement is declared effective by the SEC, the definitive proxy statement/prospectus will be mailed to the shareholders of EQV as of the record date to be established for voting on the proposed Business Combination . SECURITY HOLDERS OF EQV AND OTHER INTERESTED PARTIES ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS AND RELEVANT MATERIALS RELATING TO THE PROPOSED BUSINESS COMBINATION THAT WILL BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BEFORE MAKING ANY VOTING DECISION WITH RESPECT TO THE PROPOSED BUSINESS COMBINATION BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND THE PARTIES TO THE PROPOSED BUSINESS COMBINATION . Shareholders are able to obtain free copies of the proxy statement/prospectus and other documents containing important information about PubCo, Presidio, EQV and EQVR once such documents are filed with the SEC through the website maintained by the SEC at http : //www . sec . gov . In addition, the documents filed by EQV may be obtained free of charge from EQV at www . eqvventures . com . Alternatively, these documents, when available, can be obtained free of charge from EQV or PubCo upon written request to EQV Ventures Acquisition Corp . , 1090 Center Drive, Park City, Utah, 84098 , Attn : Secretary, or by calling ( 405 ) 870 - 3781 . The information contained on, or that may be accessed through the websites referenced in this presentation is not incorporated by reference into, and is not a part of, this presentation . Sponsor Many statements contained herein relate to the historical experience of EQV, Presidio, PubCo and EQVR, their sponsors, directors, officers, advisors, management teams and their respective current and past affiliates and investments, as applicable . An investment in EQV is not an investment in any of the past investments, companies or entities affiliated with any of the members of EQV’s, Presidio’s, PubCo’s or EQVR’s management teams or EQV’s sponsor . The historical results of these investments, companies or entities is not necessarily indicative of the future performance . Such statements do not guarantee (i) that we will be able to complete the proposed Business Combination, or (ii) success with respect to the proposed Business Combination . Trademarks This presentation also contains references to trademarks and service marks belonging to other entities. EQV and Presidio names and logos are trademarks or registered® trademarks of their respective holders. Solely for convenience, trademarks and trade names referred to in this presentation may appear without the ® or symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Use of Projections This presentation contains financial projections related to EQV, Presidio, PubCo and EQVR . Neither EQV’s, Presidio’s, PubCo’s nor EQVR’s auditors have audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and, accordingly, no such auditors have expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation . These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results . The assumptions and estimates underlying the projected information are inherently uncertain and are subject to a wide variety of significant business, regulatory, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the protected information . The assumptions underlying our projections include our ability to consummate and realize the anticipated benefits from acquisitions in the future, which may never materialize . Such acquisitions, if any, may not be consummated on the terms and conditions underlying our assumptions, and results may, and are likely to, differ materially from such assumptions . Even if the assumptions and estimates are correct, projections are inherently uncertain due to a number of factors outside EQV’s, Presidio’s, PubCo’s or EQVR’s control . Accordingly, there can be no assurance that the projected results are indicative of the future performance after the completion of any business combination or that actual results will not differ materially from those presented in the projected information . Inclusion of the projected information in this presentation should not be regarded as a representation by any person, including, without limitation, EQV, Presidio, PubCo, EQVR and any placement agent, that the results contained in the projected information will be achieved . Financial Information ; Non - GAAP Financial Measures Certain financial information and projections in this presentation for EQV, Presidio, PubCo and EQVR contain certain non - GAAP financial measures (including on a forward - looking basis), including with respect to future revenues, PV - 10 , Unlevered FCF, Unlevered FCF Yield, PDP, Dividend Yield, Leverage Ratio, Enterprise Value, Reinvestment Rate, Return on Capital Employed, Operating Cash Flow Margin, EBITDA and other non - GAAP financial measures . Please see the Glossary of this presentation for definitions of these measures . These projections of such non - GAAP financial measures cannot be confirmed with complete accuracy, and reconciliations of such projections of non - GAAP financial measures with GAAP measures are not possible to calculate . EQV, Presidio, PubCo and EQVR believe that these measures are useful to investors for the following reasons . First, EQV, Presidio, PubCo and EQVR believe that these measures may assist investors in evaluating the projected future performance and ability of the combined company to pay cash dividends to its shareholders by excluding the impact of items that do not reflect core operating performance or that are not expected to affect the ability of the combined company to pay cash dividends to its shareholders . Second, these measures are expected to be used by EQV, Presidio, PubCo and EQVR management to assess EQV’s, Presidio’s, PubCo’s and/or EQVR’s performance following completion of a Business Combination . EQV, Presidio, PubCo and EQVR believe that the future, continuing use of these non - GAAP financial measures will provide an additional tool for investors to use in evaluating ongoing operating results and trends over various reporting periods on a consistent basis . These non - GAAP financial measures should not be considered in isolation from, or as an alternative to, financial measures determined in accordance with GAAP . Other companies may calculate these non - GAAP financial measures differently, and therefore such financial measures may not be directly comparable to similarly titled measures of other companies . Please see the Glossary on page 36 for more information regarding these measures .

TABLE OF CONTENTS 3 INTRODUCTION …………………………………………………………………………………… . ………… . 4 PRESIDIO’S UNIQUE BUSINESS MODEL ……………………………… . …………… ... 16 THE RESULT ………………………………………………………………… ........................................... 27 APPENDIX … .. ………………………………………………………………… .......................................... 30

INTRODUCTION 4

A SIMPLE, DISCIPLINED APPROACH TO GENERATE STEADY INCOME FROM AMERICAN ENERGY THE PRESIDIO VISION F o u n d e d 2 0 1 7 | H e a d q u a r t e r e d i n F o r t W o r t h | 1 2 5 E m p l o y e e s 5

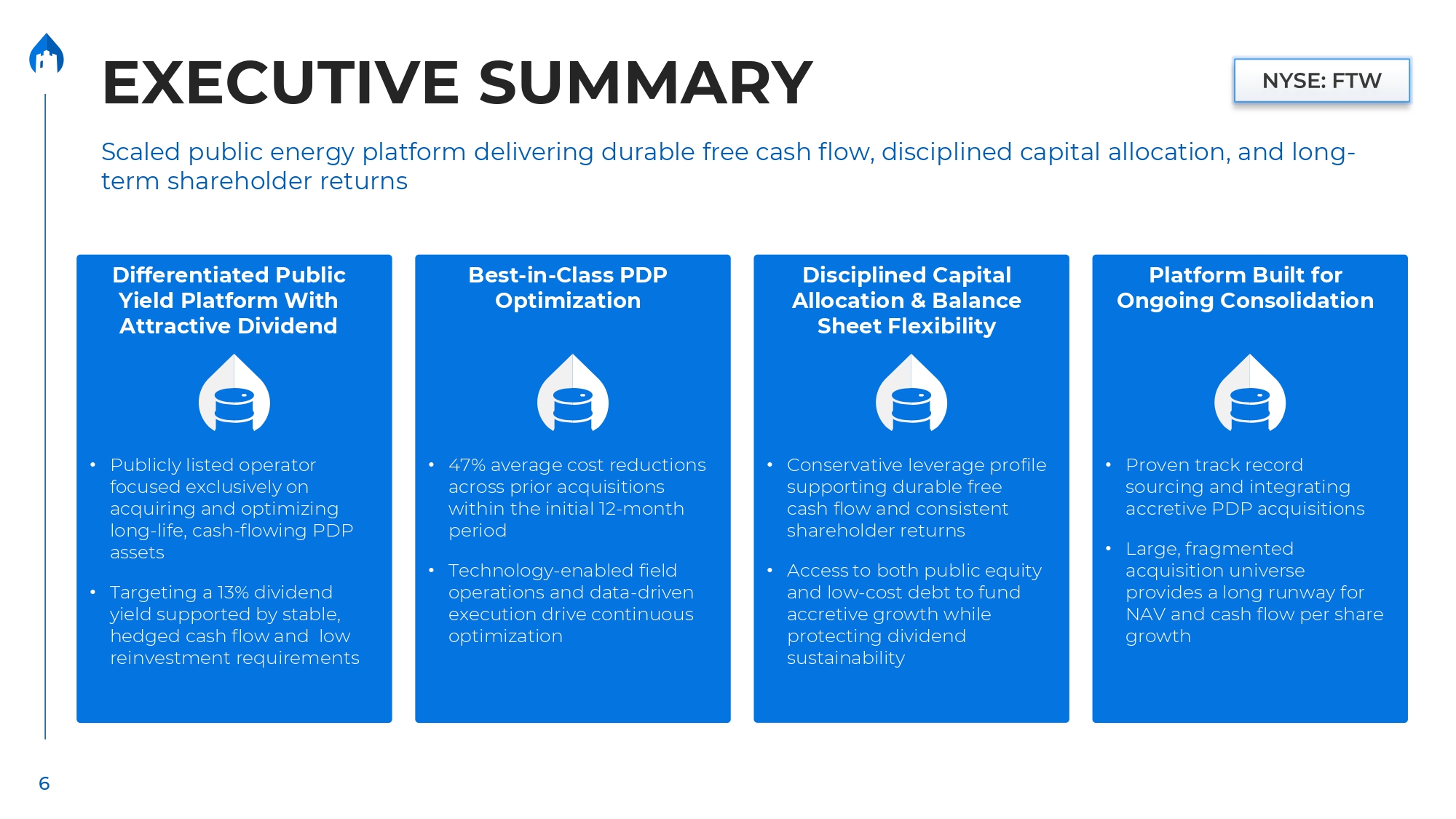

EXECUTIVE SUMMARY Platform Built for Ongoing Consolidation • Proven track record sourcing and integrating accretive PDP acquisitions • Large, fragmented acquisition universe provides a long runway for NAV and cash flow per share growth Scaled public energy platform delivering durable free cash flow, disciplined capital allocation, and long - term shareholder returns Disciplined Capital Allocation & Balance Sheet Flexibility • Conservative leverage profile supporting durable free cash flow and consistent shareholder returns • Access to both public equity and low - cost debt to fund accretive growth while protecting dividend sustainability Best - in - Class PDP Optimization • 47% average cost reductions across prior acquisitions within the initial 12 - month period • Technology - enabled field operations and data - driven execution drive continuous optimization • Publicly listed operator focused exclusively on acquiring and optimizing long - life, cash - flowing PDP assets • Targeting a 13% dividend yield supported by stable, hedged cash flow and low reinvestment requirements Differentiated Public Yield Platform With Attractive Dividend 6

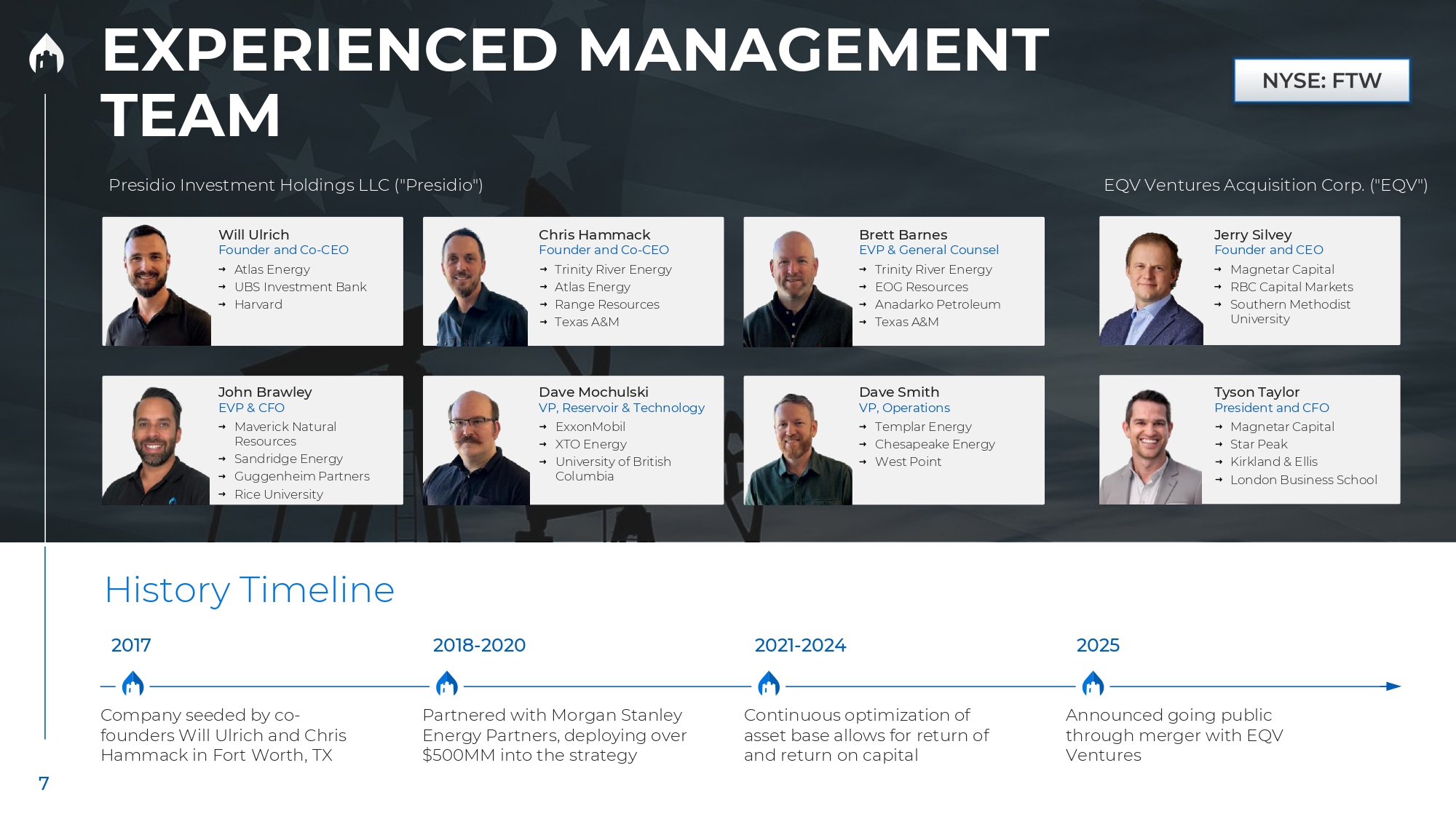

Will Ulrich Founder and Co - CEO Atlas Energy UBS Investment Bank Harvard Chris Hammack Founder and Co - CEO Trinity River Energy Atlas Energy Range Resources Texas A&M Brett Barnes EVP & General Counsel Trinity River Energy EOG Resources Anadarko Petroleum Texas A&M John Brawley EVP & CFO Maverick Natural Resources Sandridge Energy Guggenheim Partners Rice University Dave Mochulski VP, Reservoir & Technology ExxonMobil XTO Energy University of British Columbia Dave Smith VP, Operations Templar Energy Chesapeake Energy West Point EQV Ventures Acquisition Corp. ("EQV") Jerry Silvey Founder and CEO Magnetar Capital RBC Capital Markets Southern Methodist University Tyson Taylor President and CFO Magnetar Capital Star Peak Kirkland & Ellis London Business School EXPERIENCED MANAGEMENT TEAM History Timeline 2017 2018 - 2020 2021 - 2024 2025 Company seeded by co - founders Will Ulrich and Chris Hammack in Fort Worth, TX Partnered with Morgan Stanley Energy Partners, deploying over $500MM into the strategy Continuous optimization of asset base allows for return of and return on capital Announced going public through merger with EQV Ventures Presidio Investment Holdings LLC ("Presidio") 7

Ray Walker Member of Audit Committee and Nominating and Corporate Governance Committee Encino Energy, COO Range Resources ESTABLISHMENT OF A STRONG GOVERNANCE STRUCTURE Board of Directors Daniel Herz Compensation Committee Chair, Member of Audit Committee WhiteHawk Energy, CEO Falcon Minerals Corp. Atlas Energy Jerry Schretter Audit Committee Chair Bank of America, Vice Chairman and Co - Head of Americas Energy Investment Banking Cripps Leadership Advisors Citi UBS Jeff Serota Nominating and Corporate Governance Committee Chair, Member of Compensation Committee Corbel Partners, Vice Chairman and CIO Ares Management PRESIDIO IS PLEASED TO ANNOUNCE THE ADDITIONAL EXPECTED MEMBERS OF ITS BOARD James Vallee Member of Compensation Committee and Nominating and Corporate Governance Committee Winston & Strawn, Partner Valhil Capital, Valhil Advisors Paul Hastings Note: Committee assignments are subject to change prior to and following transaction close 8

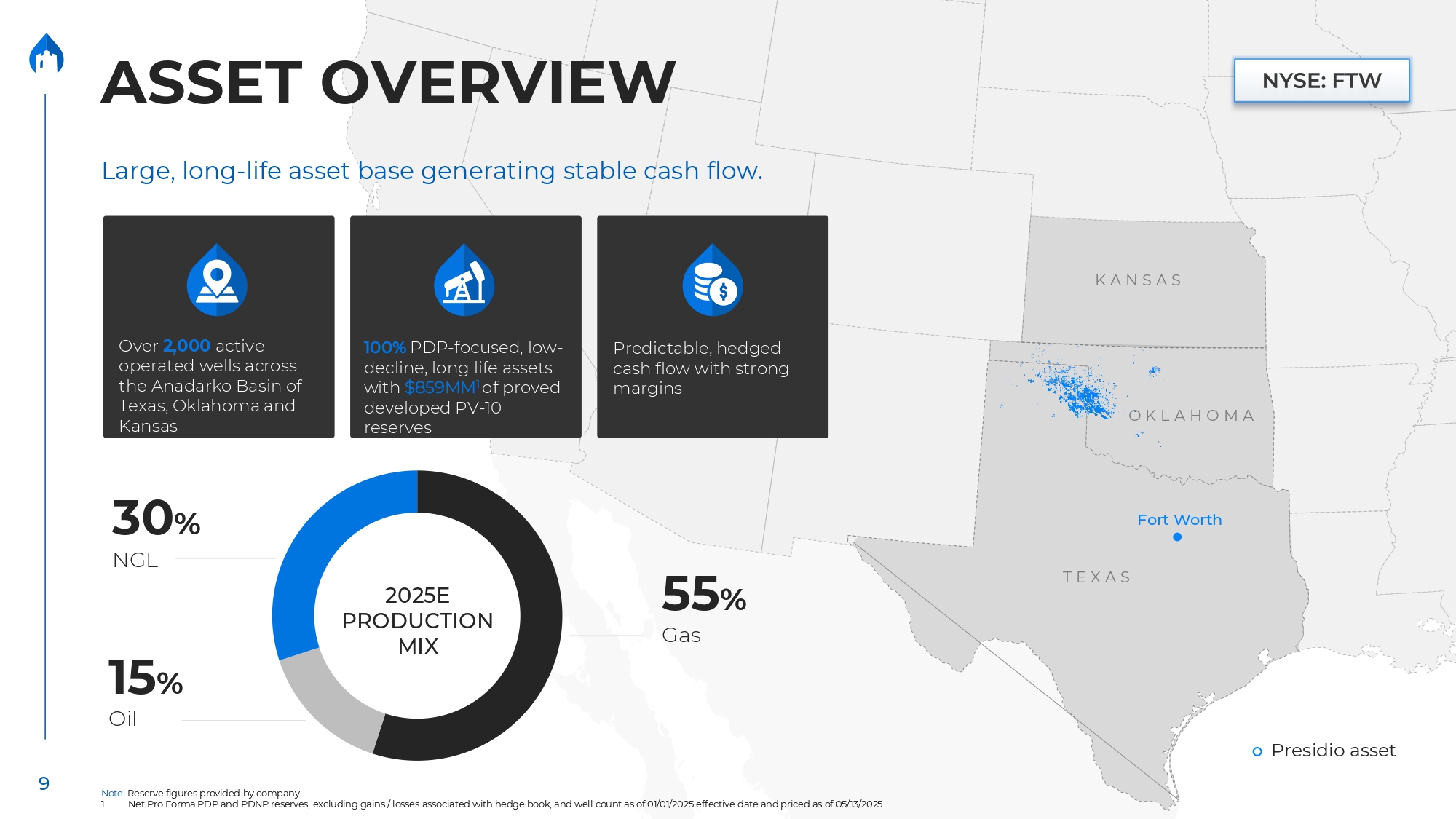

Fort Worth T E X A S O K L A H O M A K A N S A S 9 Large, long - life asset base generating stable cash flow. Presidio asset ASSET OVERVIEW Predictable, hedged cash flow with strong margins Over 2,000 active operated wells across the Anadarko Basin of Texas, Oklahoma and Kansas 100% PDP - focused, low - decline, long life assets with $859MM 1 of proved developed PV - 10 reserves 2025E PRODUCTION MIX 55 % Gas 30 % NGL 15 % Oil Note: Reserve figures provided by company 1. Net Pro Forma PDP and PDNP reserves, excluding gains / losses associated with hedge book, and well count as of 01/01/2025 effective date and priced as of 05/13/2025

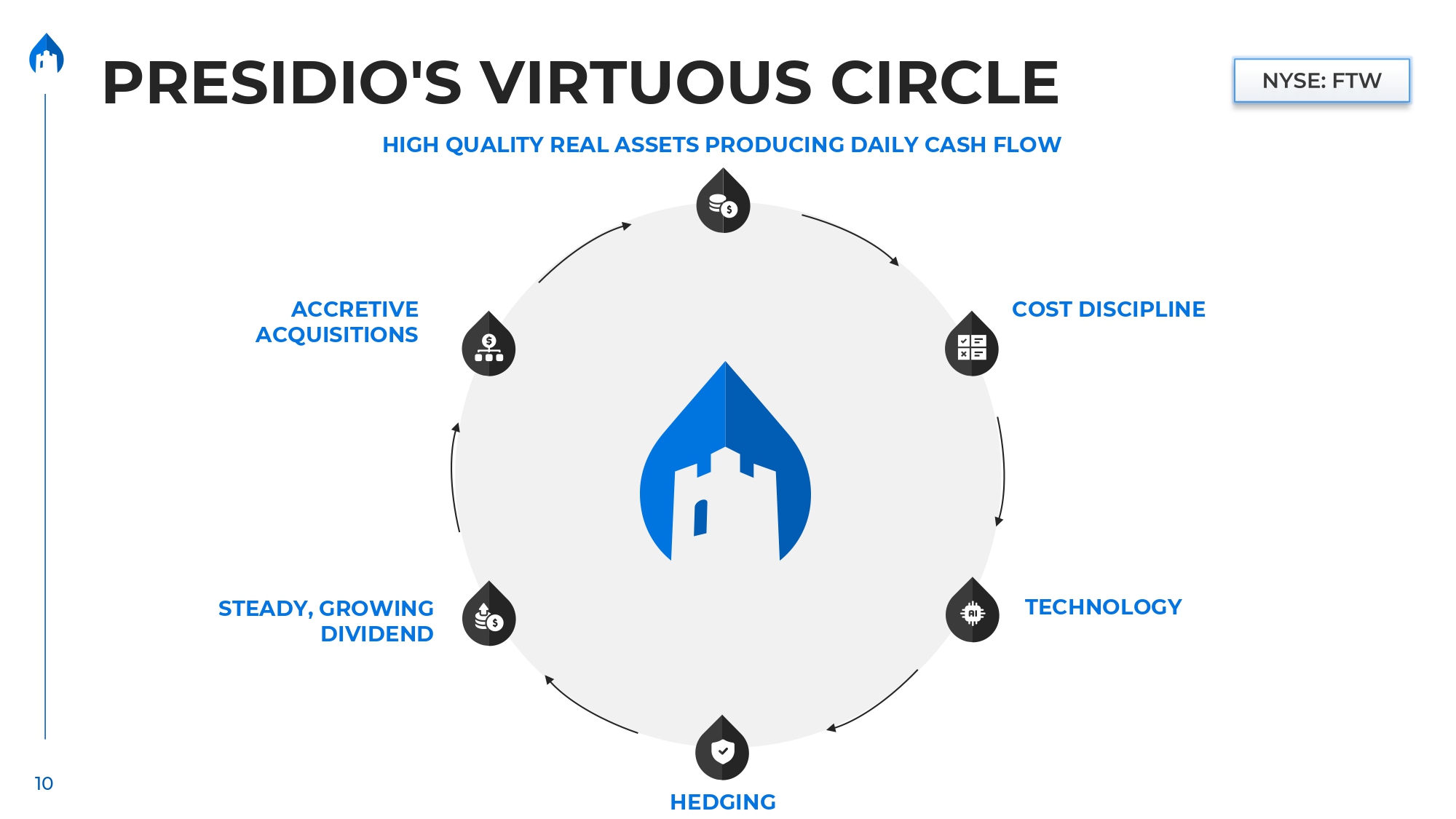

10 PRESIDIO'S VIRTUOUS CIRCLE HEDGING COST DISCIPLINE HIGH QUALITY REAL ASSETS PRODUCING DAILY CASH FLOW STEADY, GROWING DIVIDEND ACCRETIVE ACQUISITIONS TECHNOLOGY

$ 44 B RESULT 2026 - 2028 actionable pipeline 11 ACQUISITION MARKET Large Market Opportunity → Focused Where We Win FILTER I Cash - flow - positive, long - life wells $ 75 B TOTAL MARKET of PDP assets held by private equity Upstream assets held by aging PE funds expected to require liquidity within the next five years FILTER II Broadly Mid - Continent focus FILTER III Operated assets enabling cost cuts FILTER IV Next 3 years actionable pipeline

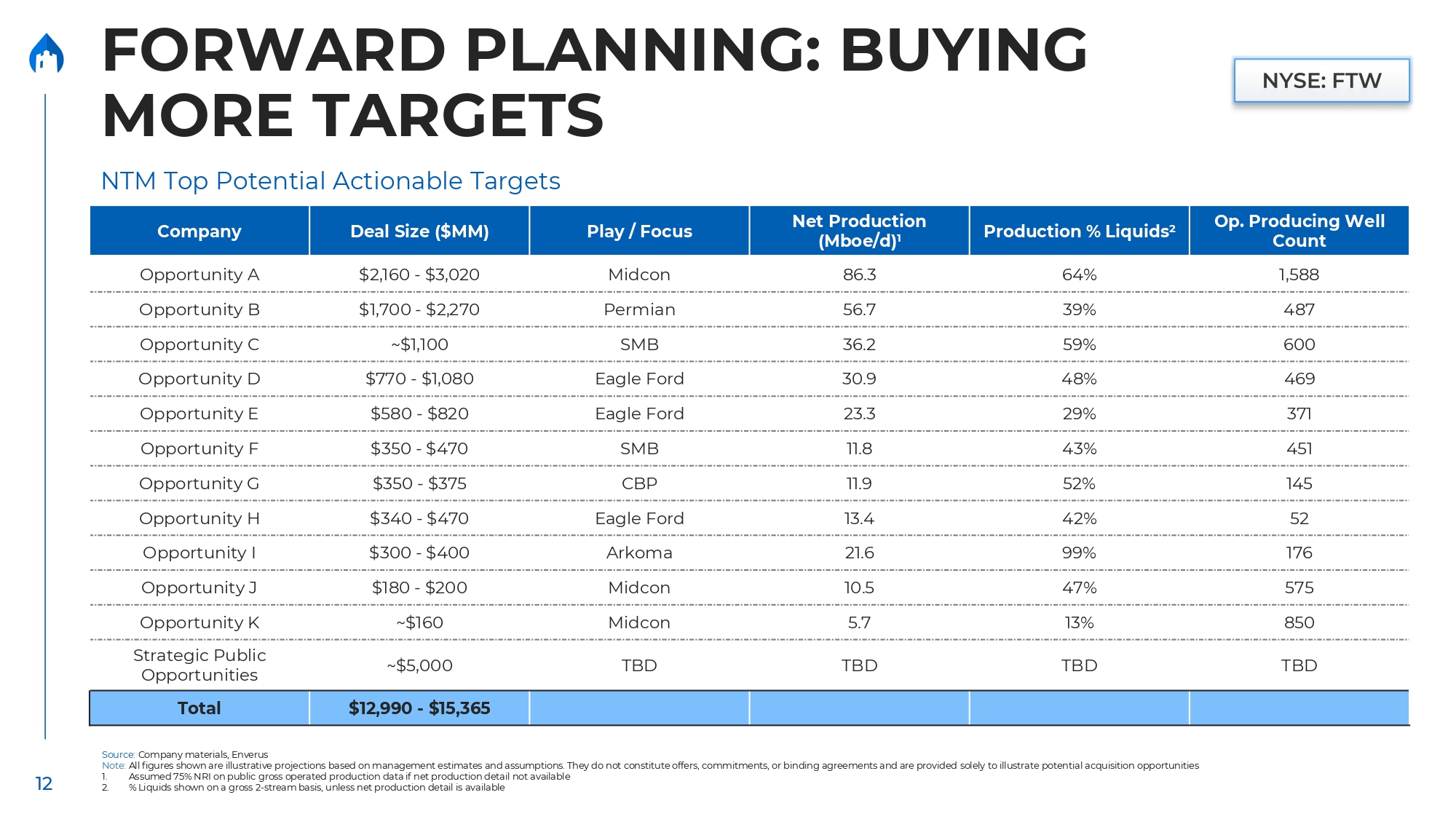

12 FORWARD PLANNING: BUYING MORE TARGETS NTM Top Potential Actionable Targets Op. Producing Well Count Production % Liquids 2 Net Production (Mboe/d) 1 Play / Focus Deal Size ($MM) Company 1,588 64% 86.3 Midcon $2,160 - $3,020 Opportunity A 487 39% 56.7 Permian $1,700 - $2,270 Opportunity B 600 59% 36.2 SMB ~$1,100 Opportunity C 469 48% 30.9 Eagle Ford $770 - $1,080 Opportunity D 371 29% 23.3 Eagle Ford $580 - $820 Opportunity E 451 43% 11.8 SMB $350 - $470 Opportunity F 145 52% 11.9 CBP $350 - $375 Opportunity G 52 42% 13.4 Eagle Ford $340 - $470 Opportunity H 176 99% 21.6 Arkoma $300 - $400 Opportunity I 575 47% 10.5 Midcon $180 - $200 Opportunity J 850 13% 5.7 Midcon ~$160 Opportunity K TBD TBD TBD TBD ~$5,000 Strategic Public Opportunities $12,990 - $15,365 Total Source: Company materials, Enverus Note: All figures shown are illustrative projections based on management estimates and assumptions. They do not constitute offers, commitments, or binding agreements and are provided solely to illustrate potential acquisition opportunities 1. Assumed 75% NRI on public gross operated production data if net production detail not available 2. % Liquids shown on a gross 2 - stream basis, unless net production detail is available

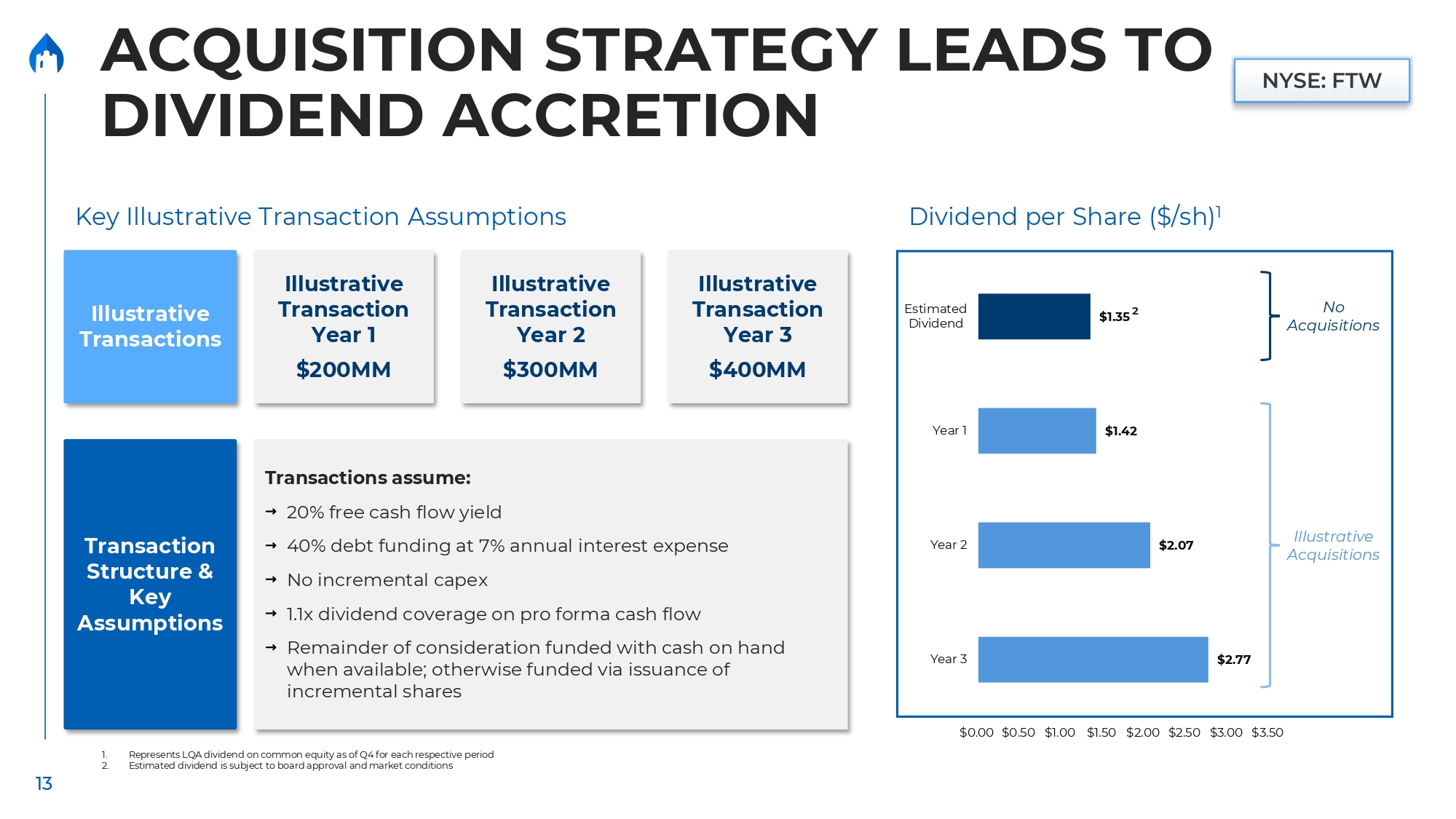

13 $2.77 $2.07 $1.42 $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 Year 3 Year 2 Year 1 Estimated Dividend No Acquisitions Illustrative Acquisitions $1.35 2 Dividend per Share ($/sh) 1 1. Represents LQA dividend on common equity as of Q4 for each respective period 2. Estimated dividend is subject to board approval and market conditions Key Illustrative Transaction Assumptions Illustrative Transaction Year 1 $200MM Transactions assume: 20% free cash flow yield 40% debt funding at 7% annual interest expense No incremental capex 1.1x dividend coverage on pro forma cash flow Remainder of consideration funded with cash on hand when available; otherwise funded via issuance of incremental shares Transaction Structure & Key Assumptions Illustrative Transactions ACQUISITION STRATEGY LEADS TO DIVIDEND ACCRETION Illustrative Transaction Year 2 $300MM Illustrative Transaction Year 3 $400MM

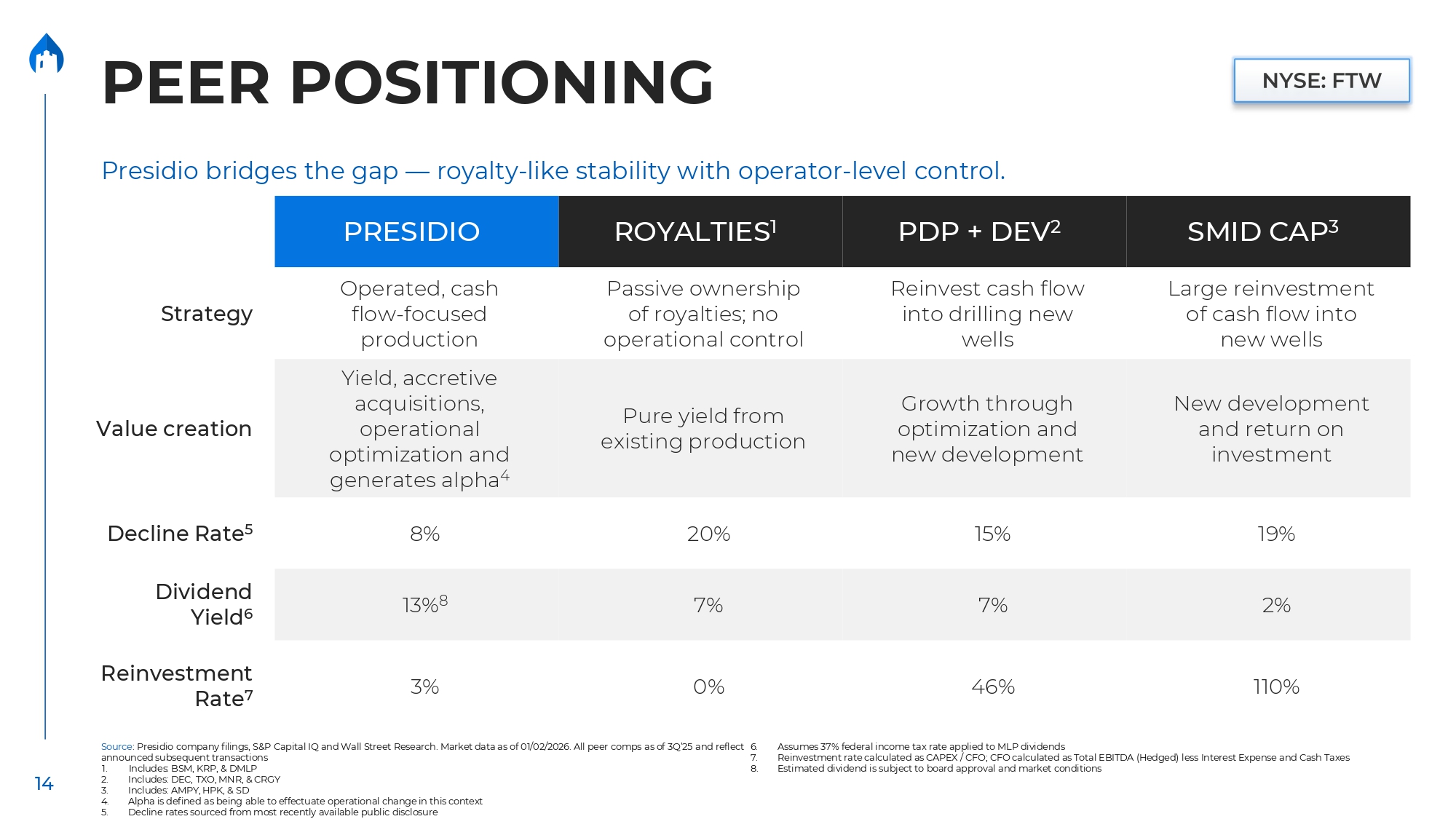

14 Presidio bridges the gap — royalty - like stability with operator - level control. announced subsequent transactions 1. Includes: BSM, KRP, & DMLP 2. Includes: DEC, TXO, MNR, & CRGY 3. Includes: AMPY, HPK, & SD 4. Alpha is defined as being able to effectuate operational change in this context 5. Decline rates sourced from most recently available public disclosure Source : Presidio company filings, S&P Capital IQ and Wall Street Research. Market data as of 01/02/2026. All peer comps as of 3Q’25 and reflect 6. Assumes 37% federal income tax rate applied to MLP dividends 7. Reinvestment rate calculated as CAPEX / CFO; CFO calculated as Total EBITDA (Hedged) less Interest Expense and Cash Taxes 8. Estimated dividend is subject to board approval and market conditions PEER POSITIONING PRESIDIO ROYALTIES 1 PDP + DEV 2 SMID CAP 3 Strategy Operated, cash flow - focused production Passive ownership of royalties; no operational control Reinvest cash flow into drilling new wells Large reinvestment of cash flow into new wells Yield, accretive Value creation New development and return on investment Growth through optimization and new development Pure yield from existing production acquisitions, operational optimization and generates alpha 4 19% 15% 20% 8% 2% 7% 7% 13% 8 110% 46% 0% 3% Decline Rate 5 Dividend Yield 6 Reinvestment Rate 7

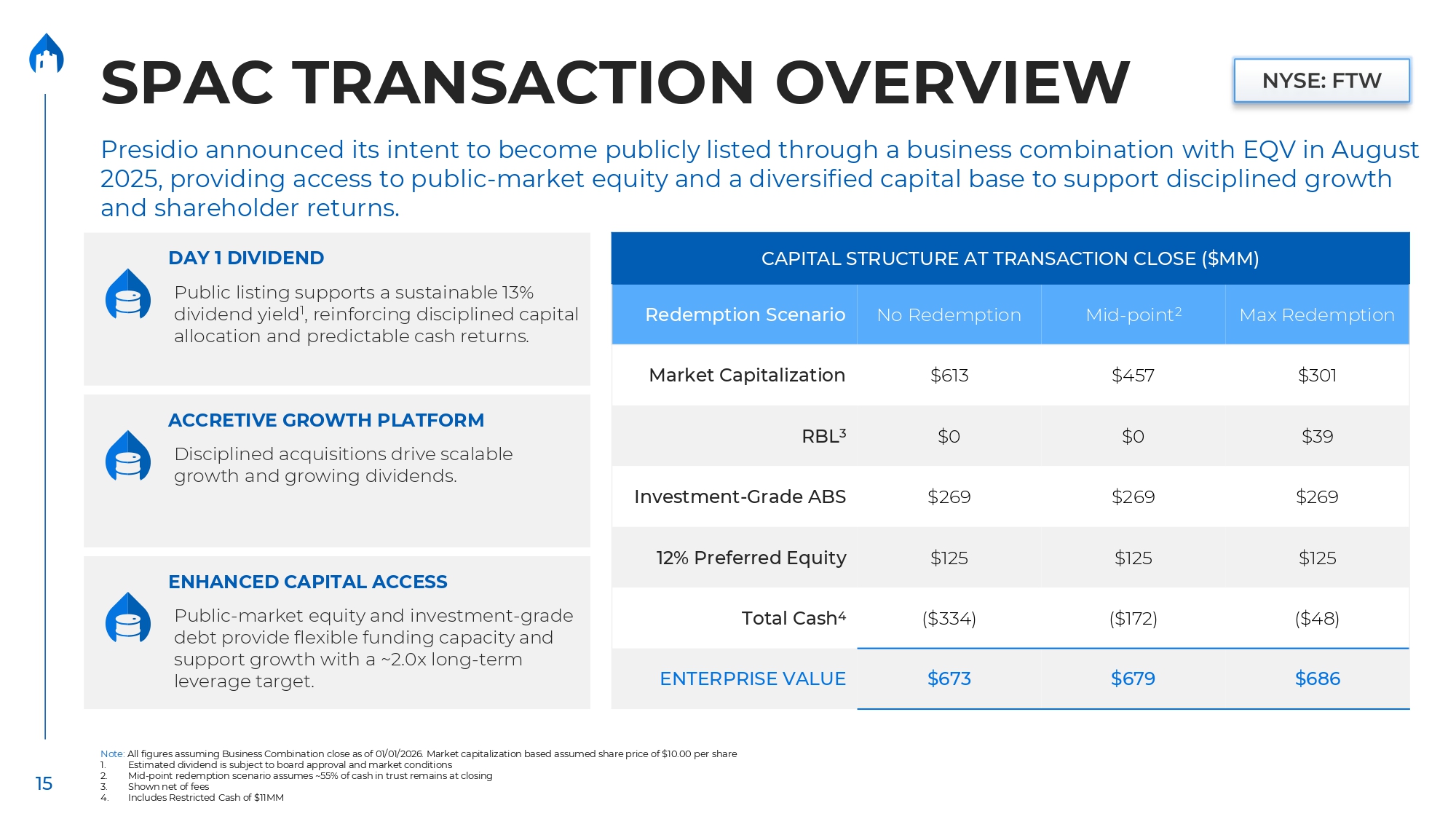

15 SPAC TRANSACTION OVERVIEW CAPITAL STRUCTURE AT TRANSACTION CLOSE ($MM) Max Redemption Mid - point 2 No Redemption Redemption Scenario $301 $457 $613 Market Capitalization $39 $0 $0 RBL 3 $269 $269 $269 Investment - Grade ABS $125 $125 $125 12% Preferred Equity ($48) ($172) ($334) Total Cash 4 $686 $679 $673 ENTERPRISE VALUE Note: All figures assuming Business Combination close as of 01/01/2026. Market capitalization based assumed share price of $10.00 per share 1. Estimated dividend is subject to board approval and market conditions 2. Mid - point redemption scenario assumes ~55% of cash in trust remains at closing 3. Shown net of fees 4. Includes Restricted Cash of $11MM Presidio announced its intent to become publicly listed through a business combination with EQV in August 2025, providing access to public - market equity and a diversified capital base to support disciplined growth and shareholder returns. DAY 1 DIVIDEND Public listing supports a sustainable 13% dividend yield 1 , reinforcing disciplined capital allocation and predictable cash returns. ACCRETIVE GROWTH PLATFORM Disciplined acquisitions drive scalable growth and growing dividends. ENHANCED CAPITAL ACCESS Public - market equity and investment - grade debt provide flexible funding capacity and support growth with a ~2.0x long - term leverage target.

PRESIDIO’S UNIQUE BUSINESS MODEL 16

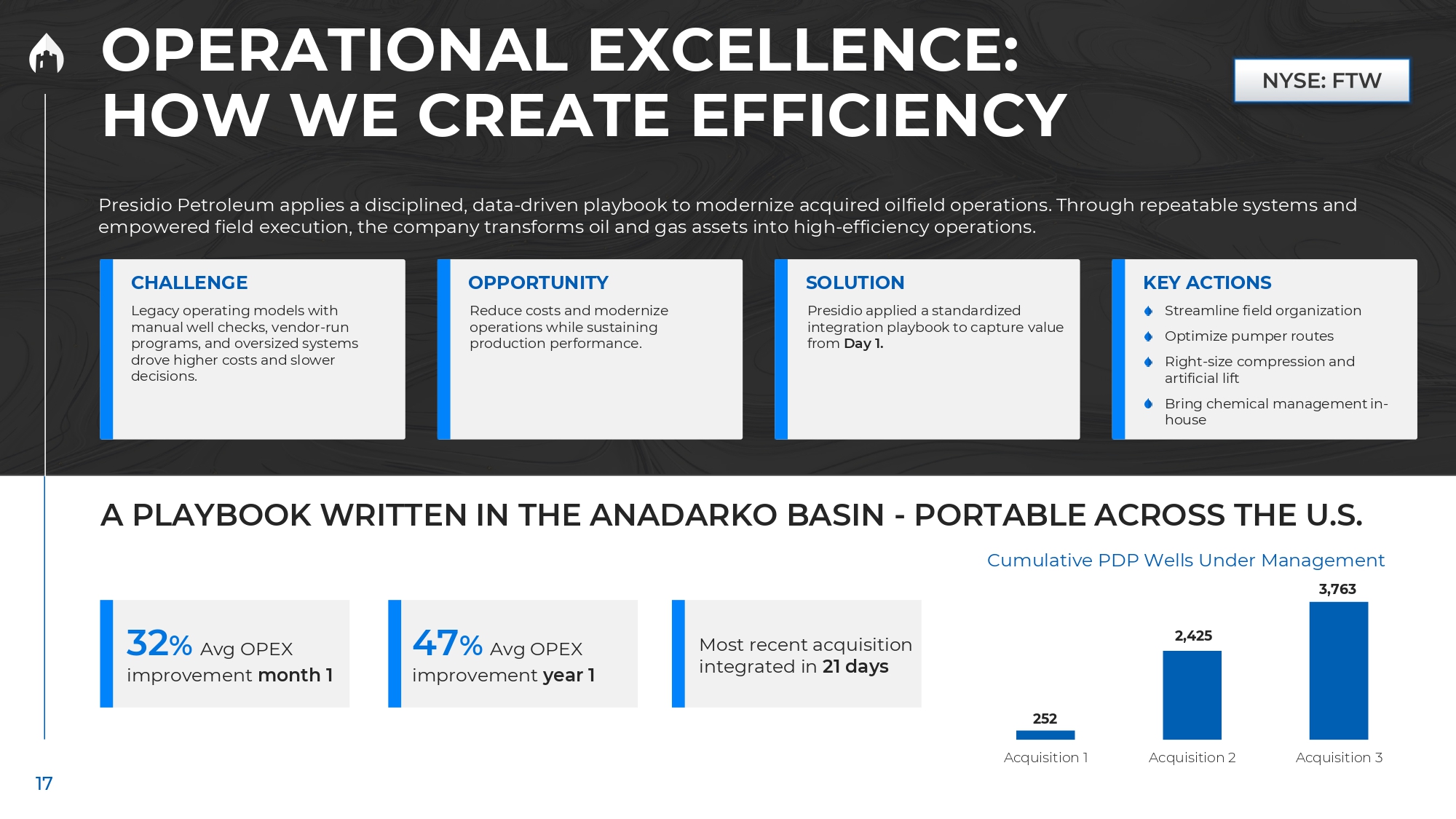

Presidio Petroleum applies a disciplined, data - driven playbook to modernize acquired oilfield operations. Through repeatable systems and empowered field execution, the company transforms oil and gas assets into high - efficiency operations. KEY ACTIONS Streamline field organization Optimize pumper routes Right - size compression and artificial lift Bring chemical management in - house CHALLENGE Legacy operating models with manual well checks, vendor - run programs, and oversized systems drove higher costs and slower decisions. SOLUTION Presidio applied a standardized integration playbook to capture value from Day 1. OPPORTUNITY Reduce costs and modernize operations while sustaining production performance. 252 2,425 Acquisition 1 Acquisition 2 Acquisition 3 32 % Avg OPEX improvement month 1 47 % Avg OPEX improvement year 1 Most recent acquisition integrated in 21 days A PLAYBOOK WRITTEN IN THE ANADARKO BASIN - PORTABLE ACROSS THE U.S. Cumulative PDP Wells Under Management 3,763 OPERATIONAL EXCELLENCE: HOW WE CREATE EFFICIENCY 17

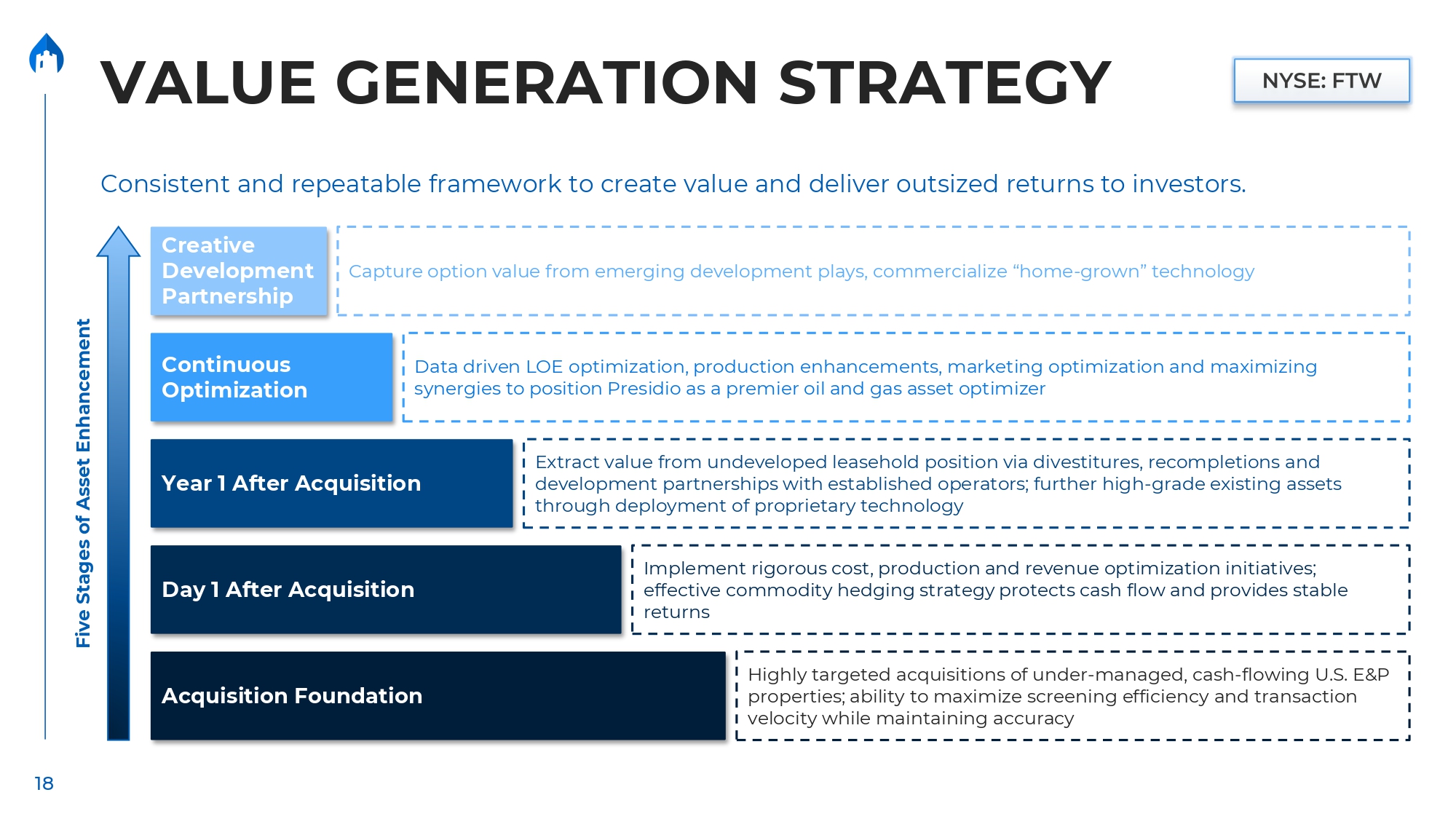

Consistent and repeatable framework to create value and deliver outsized returns to investors. Year 1 After Acquisition Extract value from undeveloped leasehold position via divestitures, recompletions and development partnerships with established operators; further high - grade existing assets through deployment of proprietary technology Day 1 After Acquisition Implement rigorous cost, production and revenue optimization initiatives; effective commodity hedging strategy protects cash flow and provides stable returns Acquisition Foundation Highly targeted acquisitions of under - managed, cash - flowing U.S. E&P properties; ability to maximize screening efficiency and transaction velocity while maintaining accuracy Continuous Optimization Data driven LOE optimization, production enhancements, marketing optimization and maximizing synergies to position Presidio as a premier oil and gas asset optimizer Creative Development Partnership Capture option value from emerging development plays, commercialize “home - grown” technology Five Stages of Asset Enhancement 18 VALUE GENERATION STRATEGY

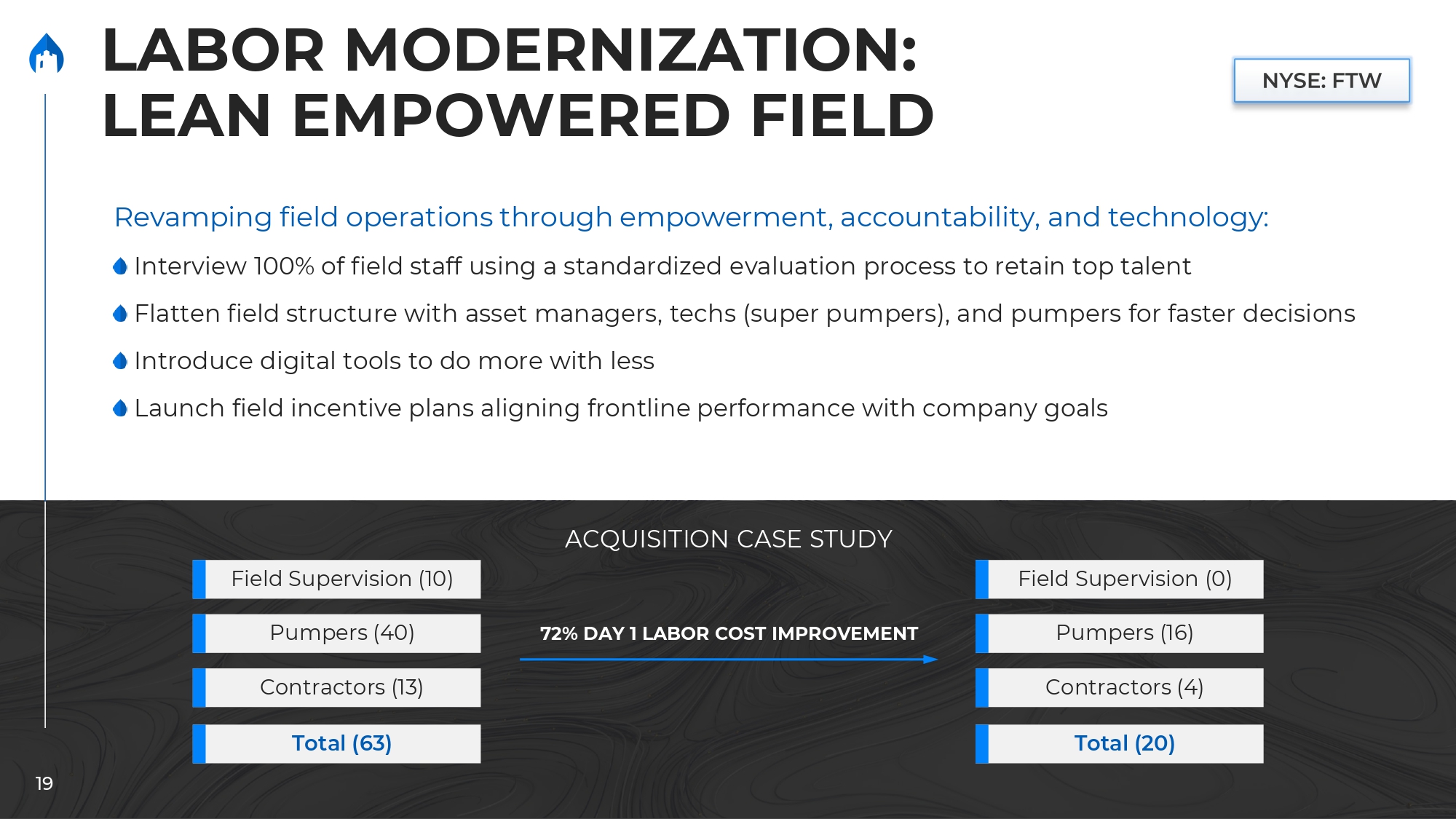

Revamping field operations through empowerment, accountability, and technology: Interview 100% of field staff using a standardized evaluation process to retain top talent Flatten field structure with asset managers, techs (super pumpers), and pumpers for faster decisions Introduce digital tools to do more with less Launch field incentive plans aligning frontline performance with company goals ACQUISITION CASE STUDY 72% DAY 1 LABOR COST IMPROVEMENT Field Supervision (10) Pumpers (40) Contractors (13) Total (63) Field Supervision (0) Pumpers (16) Contractors (4) Total (20) LABOR MODERNIZATION: LEAN EMPOWERED FIELD 19

Old Route (27 wells) New Route (50 wells) Traditional well - visit schedules gave way to an automated, exception - based system using machine learning and real - time alerting. FEWER PUMPERS High - priority wells surfaced automatically HIGHER PRODUCTIVITY Pumpers focused only where value or risk existed SMARTER ROUTES Routes adjusted dynamically based on real - time inputs PUMPER STRATEGY Legacy: Daily visits to every well PBE: Visit top 20% of wells by cash flow everyday and the rest only if alerted, resulting in 50% reduction in well visits PUMP - BY - EXCEPTION: TURNING DATA INTO FIELD ACTION 20

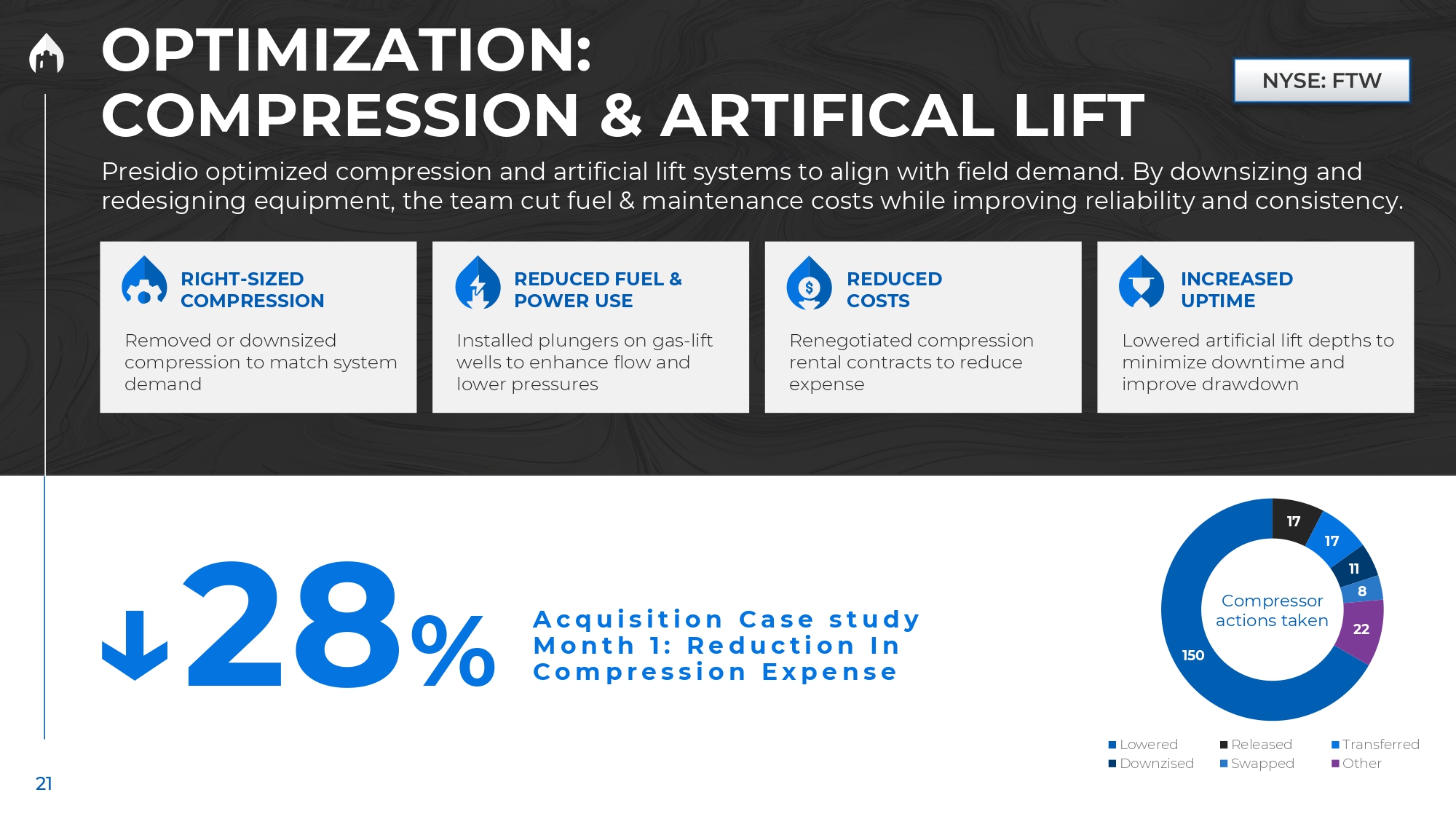

A c q u i s i t i o n C a s e s t u d y M o n t h 1 : R e d u c t i o n I n C o m p r e s s i o n E x p e n s e ↓ 28 % RIGHT - SIZED COMPRESSION Removed or downsized compression to match system demand REDUCED FUEL & POWER USE Installed plungers on gas - lift wells to enhance flow and lower pressures REDUCED COSTS Renegotiated compression rental contracts to reduce expense INCREASED UPTIME Lowered artificial lift depths to minimize downtime and improve drawdown Presidio optimized compression and artificial lift systems to align with field demand. By downsizing and redesigning equipment, the team cut fuel & maintenance costs while improving reliability and consistency. 150 17 17 11 8 22 Lowered Downzised Released Swapped Transferred Other Compressor actions taken OPTIMIZATION: 21 COMPRESSION & ARTIFICAL LIFT

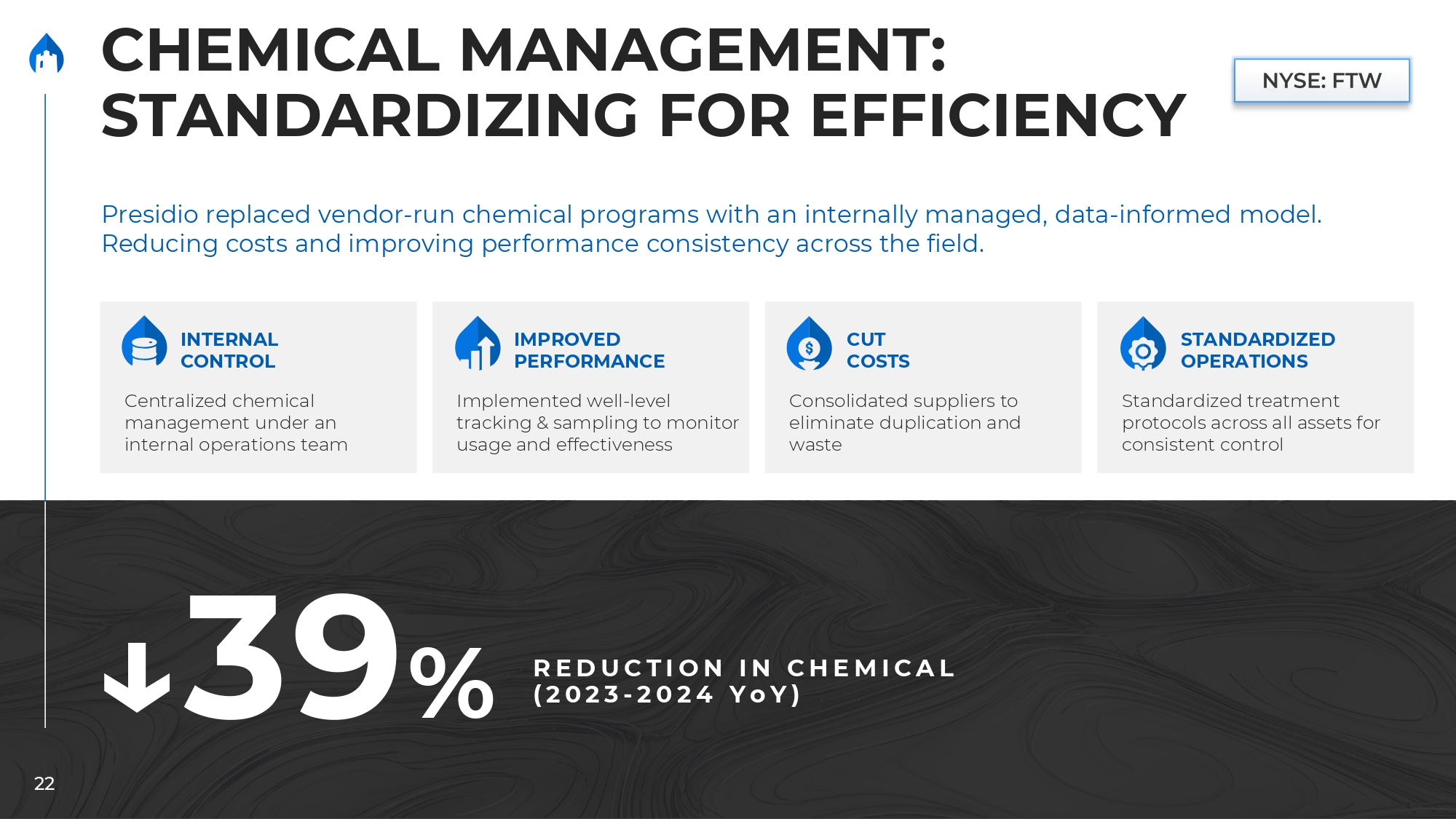

Presidio replaced vendor - run chemical programs with an internally managed, data - informed model. Reducing costs and improving performance consistency across the field. R E D U C T I O N I N C H E M I C A L ( 2 0 2 3 - 2 0 2 4 Y o Y ) ↓ 39 % INTERNAL CONTROL Centralized chemical management under an internal operations team IMPROVED PERFORMANCE Implemented well - level tracking & sampling to monitor usage and effectiveness CUT COSTS Consolidated suppliers to eliminate duplication and waste STANDARDIZED OPERATIONS Standardized treatment protocols across all assets for consistent control CHEMICAL MANAGEMENT: STANDARDIZING FOR EFFICIENCY 22

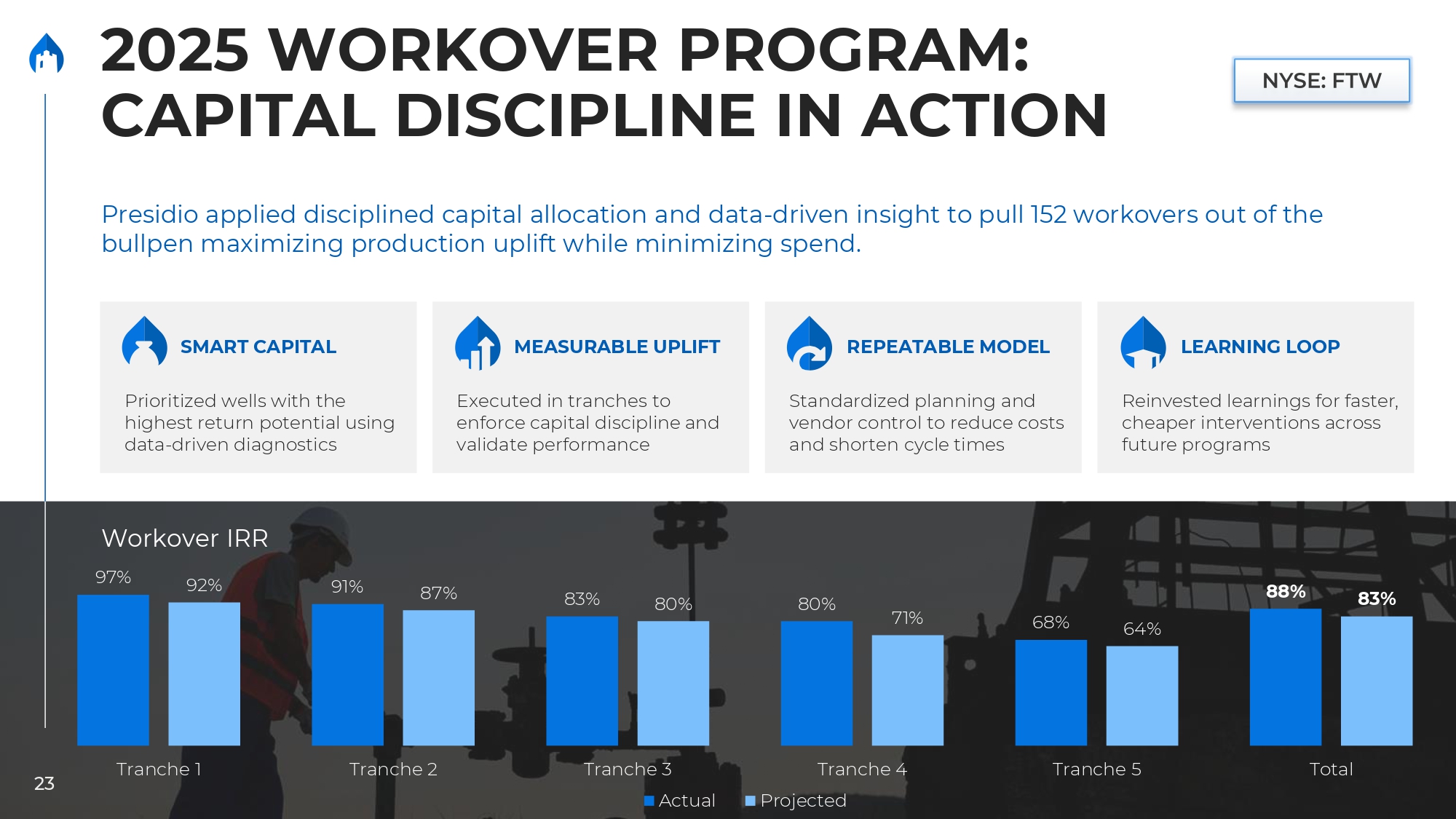

23 Presidio applied disciplined capital allocation and data - driven insight to pull 152 workovers out of the bullpen maximizing production uplift while minimizing spend. SMART CAPITAL Prioritized wells with the highest return potential using data - driven diagnostics MEASURABLE UPLIFT Executed in tranches to enforce capital discipline and validate performance REPEATABLE MODEL Standardized planning and vendor control to reduce costs and shorten cycle times LEARNING LOOP Reinvested learnings for faster, cheaper interventions across future programs Workover IRR 97% 91% 83% 80% 68% 88% 92% 87% 80% 71% 64% 83% Tranche 1 Tranche 2 Tranche 5 Total Tranche 3 Actual Tranche 4 Projected 2025 WORKOVER PROGRAM: CAPITAL DISCIPLINE IN ACTION

24 DEVELOPMENT: BRINGING VALUE FORWARD Over $100MM in value realized with zero capital risk. Flexible capital and operating structures allow Presidio to scale with partners and deliver growth without incremental overhead or risk. STRUCTURED JOINT VENTURES Built and executed JV frameworks where partners fund drilling programs and Presidio assumes operatorship post - development, supporting long - term efficiency and alignment. ACREAGE SALES Executed strategic acreage sales, including ~100k acres in the Cherokee formation, to realize value while retaining existing wells and further upside. OUTSOURCED DEVELOPMENT MANAGEMENT Successfully managed development programs funded and executed by partners, promoting timely project completion, reducing cost structure, and heightening operating standards. CASE STUDY — FARM - OUT (CARRIED DEVELOPMENT PROGRAM) • Structured carry where partner funded and drilled initial wells and Presidio contributed acreage. • Presidio assumed operatorship upon completion. • Delivered low - cost transition, and long - term cash flow alignment.

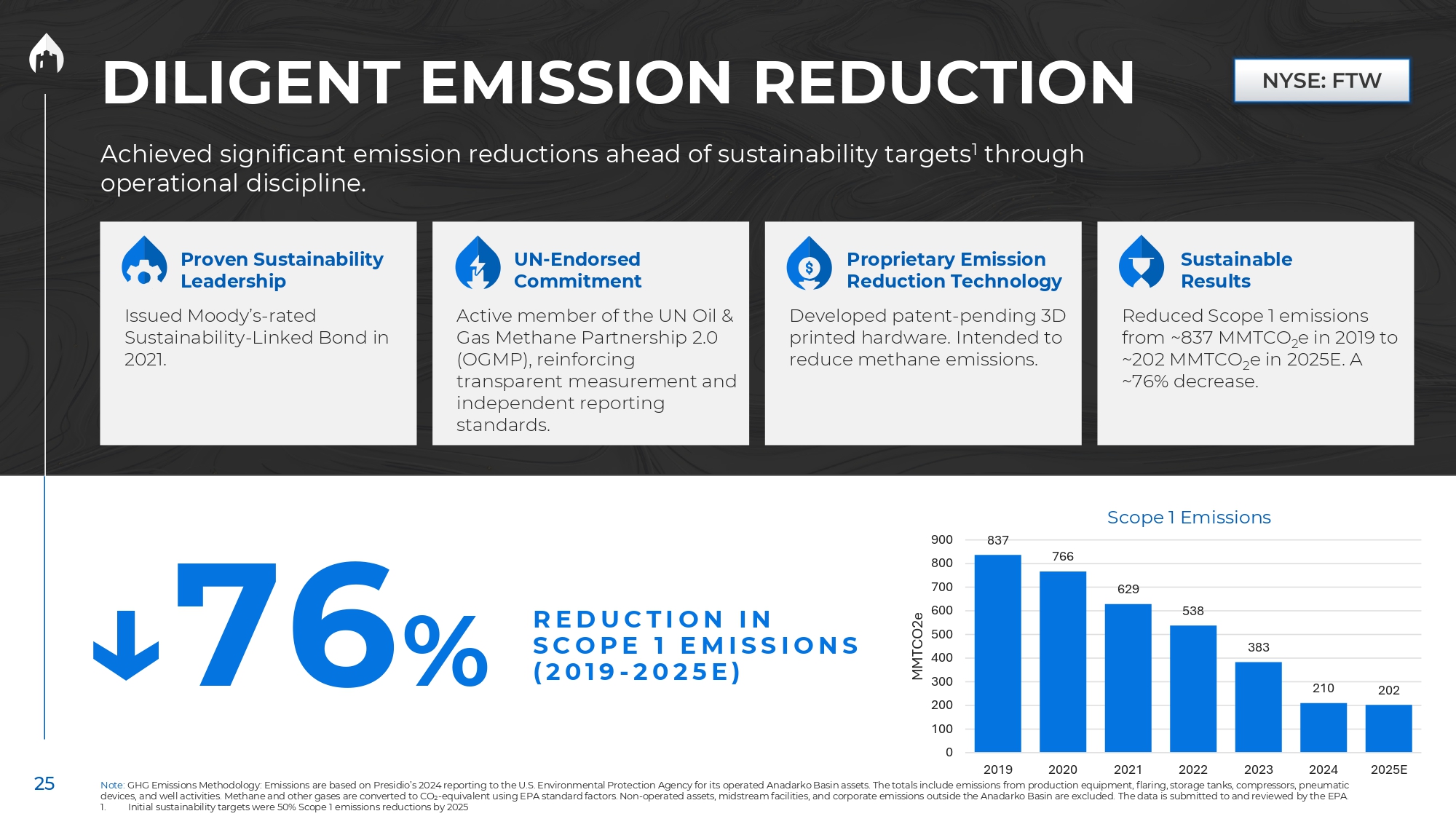

25 837 766 629 538 383 210 202 900 800 700 600 500 400 300 200 100 0 2025E MMTCO2e R E D U C T I O N I N S C O P E 1 E M I S S I O N S ( 2 0 1 9 - 2 0 2 5 E ) ↓ 76 % Proven Sustainability Leadership Issued Moody’s - rated Sustainability - Linked Bond in 2021. UN - Endorsed Commitment Active member of the UN Oil & Gas Methane Partnership 2.0 (OGMP), reinforcing transparent measurement and independent reporting standards. Proprietary Emission Reduction Technology Developed patent - pending 3 D printed hardware . Intended to reduce methane emissions . Sustainable Results Reduced Scope 1 emissions from ~837 MMTCO 2 e in 2019 to ~202 MMTCO 2 e in 2025E. A ~76% decrease. DILIGENT EMISSION REDUCTION Achieved significant emission reductions ahead of sustainability targets 1 through operational discipline. Scope 1 Emissions 2019 2020 2021 2022 2023 2024 Note: GHG Emissions Methodology: Emissions are based on Presidio’s 2024 reporting to the U.S. Environmental Protection Agency for its operated Anadarko Basin assets. The totals include emissions from production equipment, flaring, storage tanks, compressors, pneumatic devices, and well activities. Methane and other gases are converted to CO₂ - equivalent using EPA standard factors. Non - operated assets, midstream facilities, and corporate emissions outside the Anadarko Basin are excluded. The data is submitted to and reviewed by the EPA. 1. Initial sustainability targets were 50% Scope 1 emissions reductions by 2025

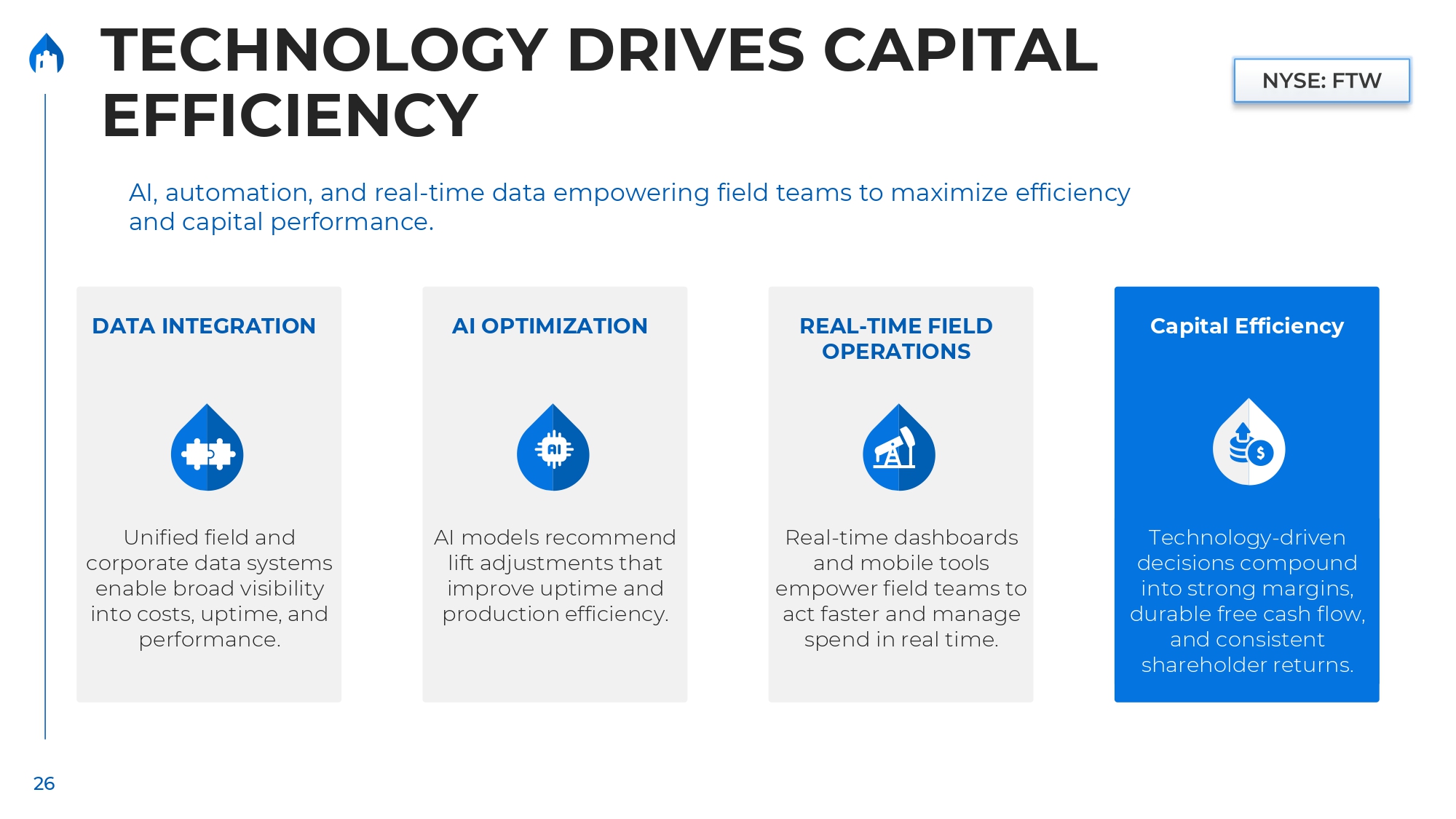

TECHNOLOGY DRIVES CAPITAL EFFICIENCY Unified field and corporate data systems enable broad visibility into costs, uptime, and performance. DATA INTEGRATION AI models recommend lift adjustments that improve uptime and production efficiency. AI OPTIMIZATION Real - time dashboards and mobile tools empower field teams to act faster and manage spend in real time. REAL - TIME FIELD OPERATIONS Technology - driven decisions compound into strong margins, durable free cash flow, and consistent shareholder returns. Capital Efficiency AI, automation, and real - time data empowering field teams to maximize efficiency and capital performance. 26

THE RESULT 27

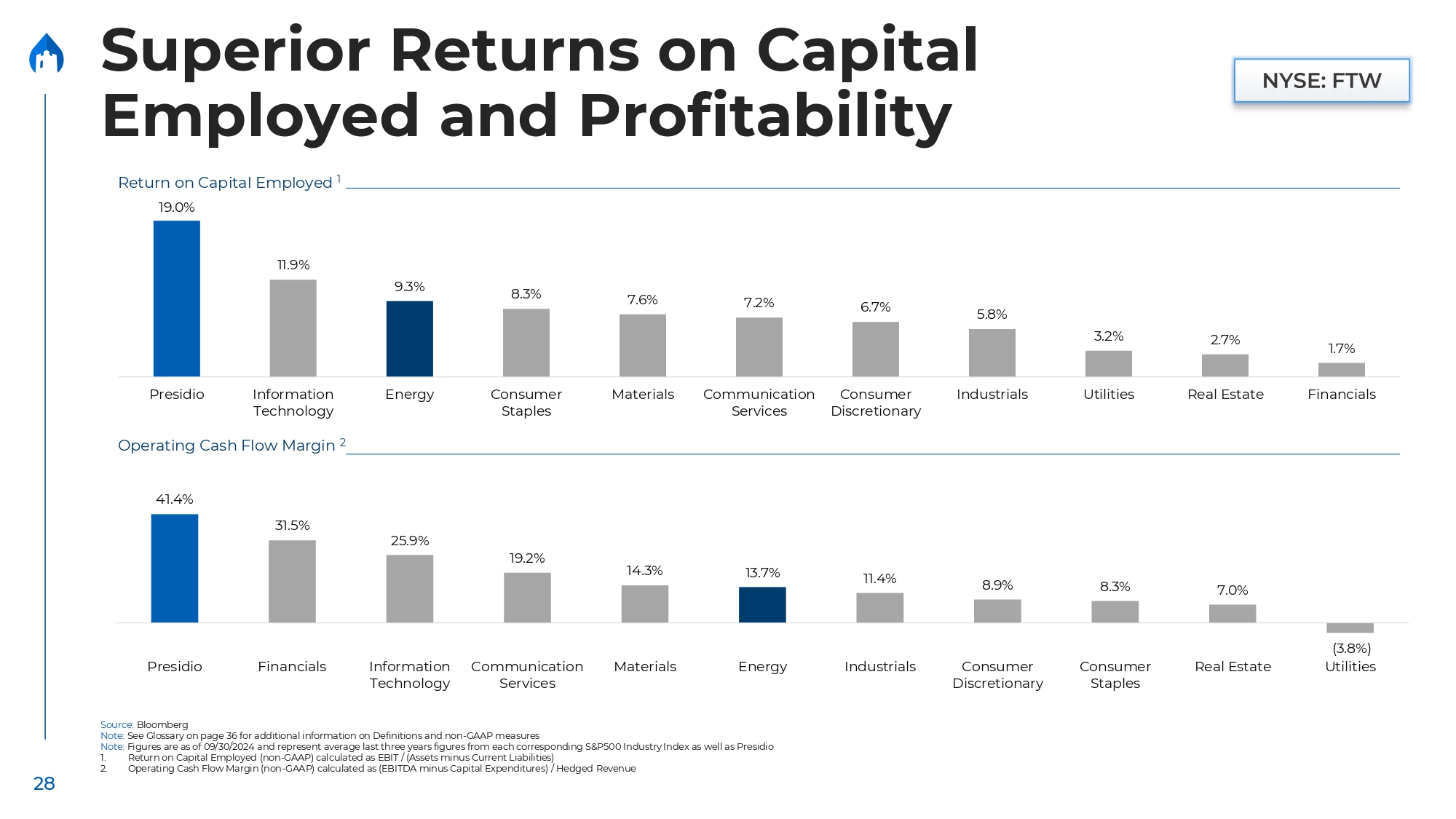

Superior Returns on Capital Employed and Profitability Source: Bloomberg Note: See Glossary on page 36 for additional information on Definitions and non - GAAP measures Note: Figures are as of 09/30/2024 and represent average last three years figures from each corresponding S&P500 Industry Index as well as Presidio 1. Return on Capital Employed (non - GAAP) calculated as EBIT / (Assets minus Current Liabilities) 2. Operating Cash Flow Margin (non - GAAP) calculated as (EBITDA minus Capital Expenditures) / Hedged Revenue 1.7% 2.7% 3.2% 5.8% 6.7% 7.2% 7.6% 8.3% 9.3% 11.9% Return on Capital Employed 1 19.0% Financials Real Estate Utilities Industrials Consumer Discretionary Communication Services Materials Consumer Staples Energy Information Technology Presidio (3.8%) Utilities 7.0% 8.3% 8.9% 11.4% 13.7% 14.3% Operating Cash Flow Margin 2 41.4% 31.5% 25.9% 19.2% Real Estate Consumer Staples Consumer Discretionary Industrials Energy Materials Communication Services Information Technology Financials Presidio 28

Presidio’ s scalable model, disciplined operations, and integrated systems position the company as a trusted operator for long - term growth and partnership Significant existing well count with proven ability to scale Proven optimization track record Access to growth capital through public equity and investment - grade debt Ability to acquire assets over time Advanced cloud - based systems and AI implementation A PROVEN, SCALABLE PLATFORM 29

APPENDIX 30

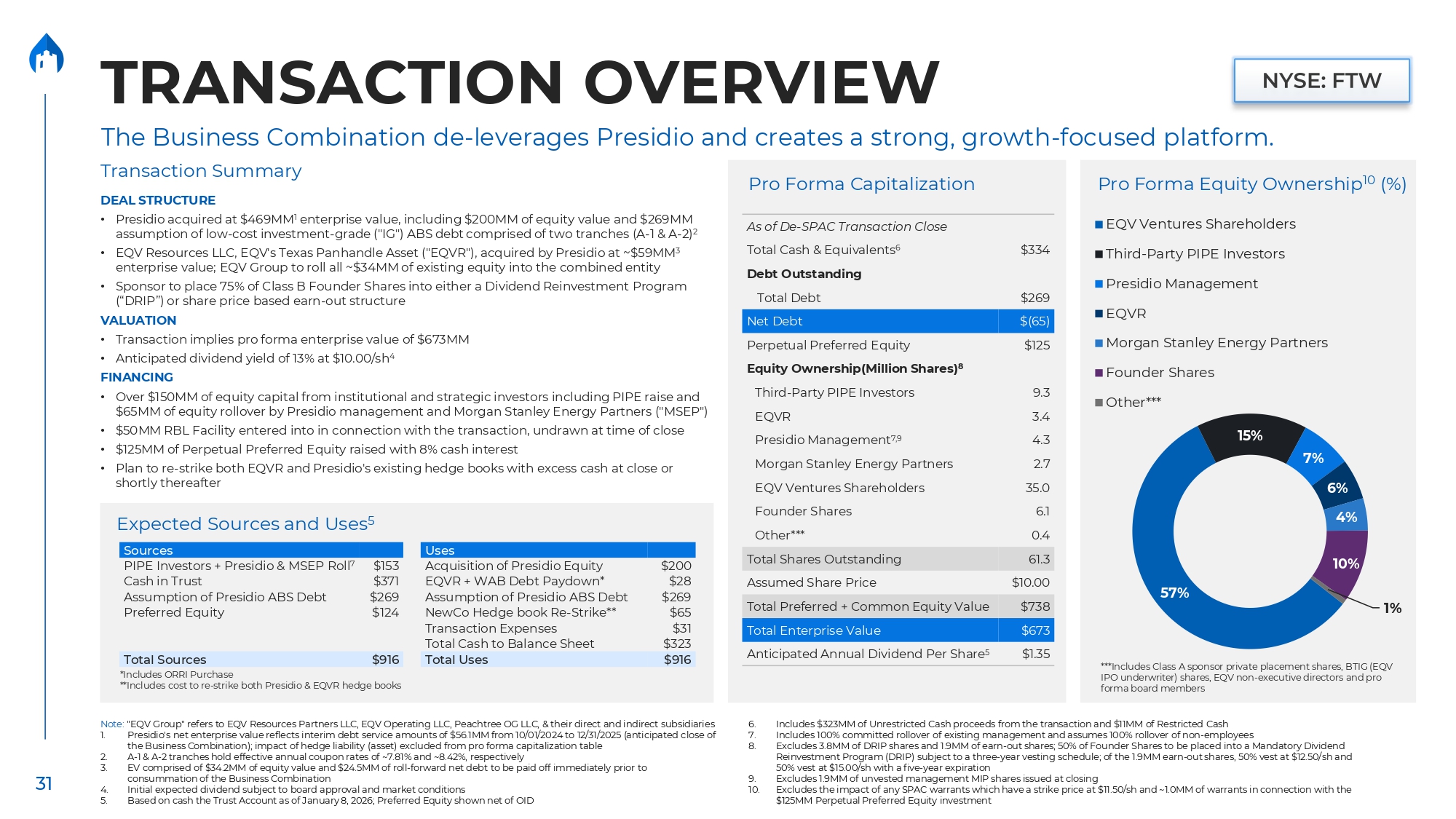

31 The Business Combination de - leverages Presidio and creates a strong, growth - focused platform. Transaction Summary DEAL STRUCTURE Pro Forma Equity Ownership 10 (%) EQV Ventures Shareholders Third - Party PIPE Investors Presidio Management EQVR Morgan Stanley Energy Partners Founder Shares Other*** 15% 7% 6% 4% 10% 57% 1% ***Includes Class A sponsor private placement shares, BTIG (EQV IPO underwriter) shares, EQV non - executive directors and pro forma board members • Presidio acquired at $469MM 1 enterprise value, including $200MM of equity value and $269MM assumption of low - cost investment - grade ("IG") ABS debt comprised of two tranches (A - 1 & A - 2) 2 • EQV Resources LLC, EQV's Texas Panhandle Asset ("EQVR"), acquired by Presidio at ~$59MM 3 enterprise value; EQV Group to roll all ~$34MM of existing equity into the combined entity • Sponsor to place 75% of Class B Founder Shares into either a Dividend Reinvestment Program (“DRIP”) or share price based earn - out structure VALUATION • Transaction implies pro forma enterprise value of $673MM • Anticipated dividend yield of 13% at $10.00/sh 4 FINANCING • Over $150MM of equity capital from institutional and strategic investors including PIPE raise and $65MM of equity rollover by Presidio management and Morgan Stanley Energy Partners ("MSEP") • $50MM RBL Facility entered into in connection with the transaction, undrawn at time of close • $125MM of Perpetual Preferred Equity raised with 8% cash interest • Plan to re - strike both EQVR and Presidio's existing hedge books with excess cash at close or shortly thereafter Uses Expected Sources and Uses 5 Sources PIPE Investors + Presidio & MSEP Roll 7 $153 Acquisition of Presidio Equity Cash in Trust $371 EQVR + WAB Debt Paydown* Assumption of Presidio ABS Debt $269 Assumption of Presidio ABS Debt Preferred Equity $124 NewCo Hedge book Re - Strike** Transaction Expenses Total Cash to Balance Sheet $200 $28 $269 $65 $31 $323 Total Sources $916 Total Uses $916 $334 Pro Forma Capitalization As of De - SPAC Transaction Close Total Cash & Equivalents 6 Debt Outstanding Total Debt Net Debt Perpetual Preferred Equity Equity Ownership(Million Shares) 8 Third - Party PIPE Investors EQVR Presidio Management 7,9 Morgan Stanley Energy Partners EQV Ventures Shareholders Founder Shares Other*** $269 $(65) $125 9.3 3.4 4.3 2.7 35.0 6.1 0.4 Total Shares Outstanding 61.3 Assumed Share Price $ 10 . 00 Total Preferred + Common Equity Value $ 738 Total Enterprise Value $ 673 Anticipated Annual Dividend Per Share 5 $ 1 . 35 *Includes ORRI Purchase **Includes cost to re - strike both Presidio & EQVR hedge books Note: "EQV Group" refers to EQV Resources Partners LLC, EQV Operating LLC, Peachtree OG LLC, & their direct and indirect subsidiaries 1. Presidio's net enterprise value reflects interim debt service amounts of $56.1MM from 10/01/2024 to 12/31/2025 (anticipated close of the Business Combination); impact of hedge liability (asset) excluded from pro forma capitalization table 2. A - 1 & A - 2 tranches hold effective annual coupon rates of ~7.81% and ~8.42%, respectively 3. EV comprised of $34.2MM of equity value and $24.5MM of roll - forward net debt to be paid off immediately prior to consummation of the Business Combination 4. Initial expected dividend subject to board approval and market conditions 5. Based on cash the Trust Account as of January 8, 2026; Preferred Equity shown net of OID 6. Includes $323MM of Unrestricted Cash proceeds from the transaction and $11MM of Restricted Cash 7. Includes 100% committed rollover of existing management and assumes 100% rollover of non - employees 8. Excludes 3.8MM of DRIP shares and 1.9MM of earn - out shares; 50% of Founder Shares to be placed into a Mandatory Dividend Reinvestment Program (DRIP) subject to a three - year vesting schedule; of the 1.9MM earn - out shares, 50% vest at $12.50/sh and 50% vest at $15.00/sh with a five - year expiration 9. Excludes 1.9MM of unvested management MIP shares issued at closing 10. Excludes the impact of any SPAC warrants which have a strike price at $11.50/sh and ~1.0MM of warrants in connection with the $125MM Perpetual Preferred Equity investment TRANSACTION OVERVIEW

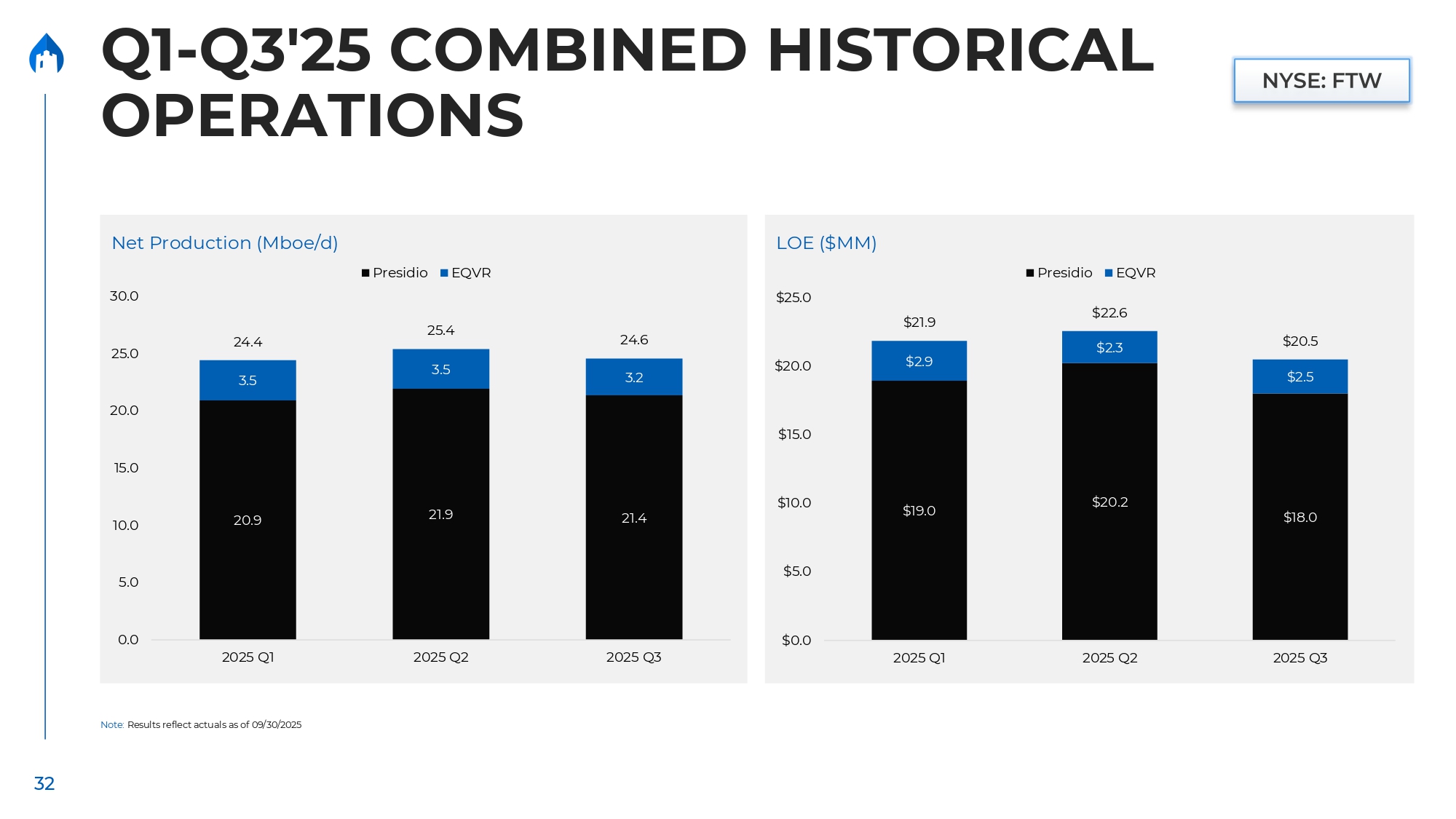

32 Net Production (Mboe/d) 20.9 21.9 21.4 3.5 3.5 3.2 24.4 25.4 24.6 0.0 5.0 10.0 15.0 20.0 25.0 30.0 2025 Q1 2025 Q2 2025 Q3 Presidio EQVR LOE ($MM) $19.0 $20.2 $18.0 $2.9 $2.5 $21.9 $22.6 $2.3 $20.5 $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 2025 Q1 2025 Q2 2025 Q3 Presidio EQVR Q1 - Q3'25 COMBINED HISTORICAL OPERATIONS Note: Results reflect actuals as of 09/30/2025

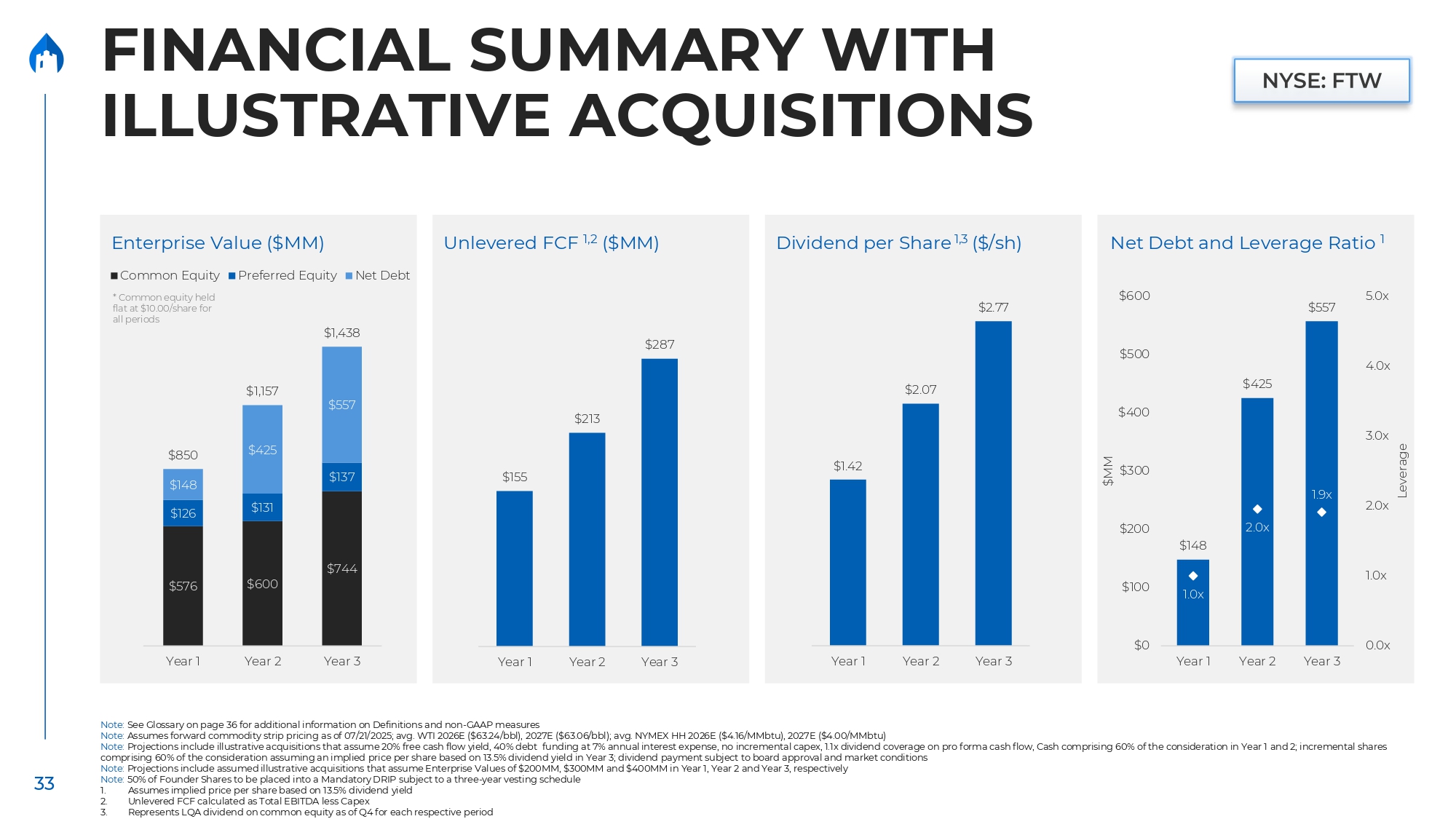

33 $576 $600 $744 $126 $131 $137 $148 $425 $557 $850 $1,157 Year 1 Year 2 Year 3 Enterprise Value ($MM) Common Equity Preferred Equity Net Debt * Common equity held flat at $10.00/share for all periods $1,438 Unlevered FCF 1,2 ($MM) $155 $213 $287 Year 1 Year 2 Year 3 Dividend per Share 1,3 ($/sh) Net Debt and Leverage Ratio 1 $1.42 $2.07 $2.77 Year 1 Year 2 Year 3 $148 $425 $557 1.0x 2.0x 1.9x 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x $0 $100 $200 $300 $400 $500 $600 Year 1 Year 2 Year 3 Leverage $MM FINANCIAL SUMMARY WITH ILLUSTRATIVE ACQUISITIONS Note: See Glossary on page 36 for additional information on Definitions and non - GAAP measures Note: Assumes forward commodity strip pricing as of 07/21/2025; avg. WTI 2026E ($63.24/bbl), 2027E ($63.06/bbl); avg. NYMEX HH 2026E ($4.16/MMbtu), 2027E ($4.00/MMbtu) Note: Projections include illustrative acquisitions that assume 20% free cash flow yield, 40% debt funding at 7% annual interest expense, no incremental capex, 1.1x dividend coverage on pro forma cash flow, Cash comprising 60% of the consideration in Year 1 and 2; incremental shares comprising 60% of the consideration assuming an implied price per share based on 13.5% dividend yield in Year 3; dividend payment subject to board approval and market conditions Note: Projections include assumed illustrative acquisitions that assume Enterprise Values of $200MM, $300MM and $400MM in Year 1, Year 2 and Year 3, respectively Note: 50% of Founder Shares to be placed into a Mandatory DRIP subject to a three - year vesting schedule 1. Assumes implied price per share based on 13.5% dividend yield 2. Unlevered FCF calculated as Total EBITDA less Capex 3. Represents LQA dividend on common equity as of Q4 for each respective period

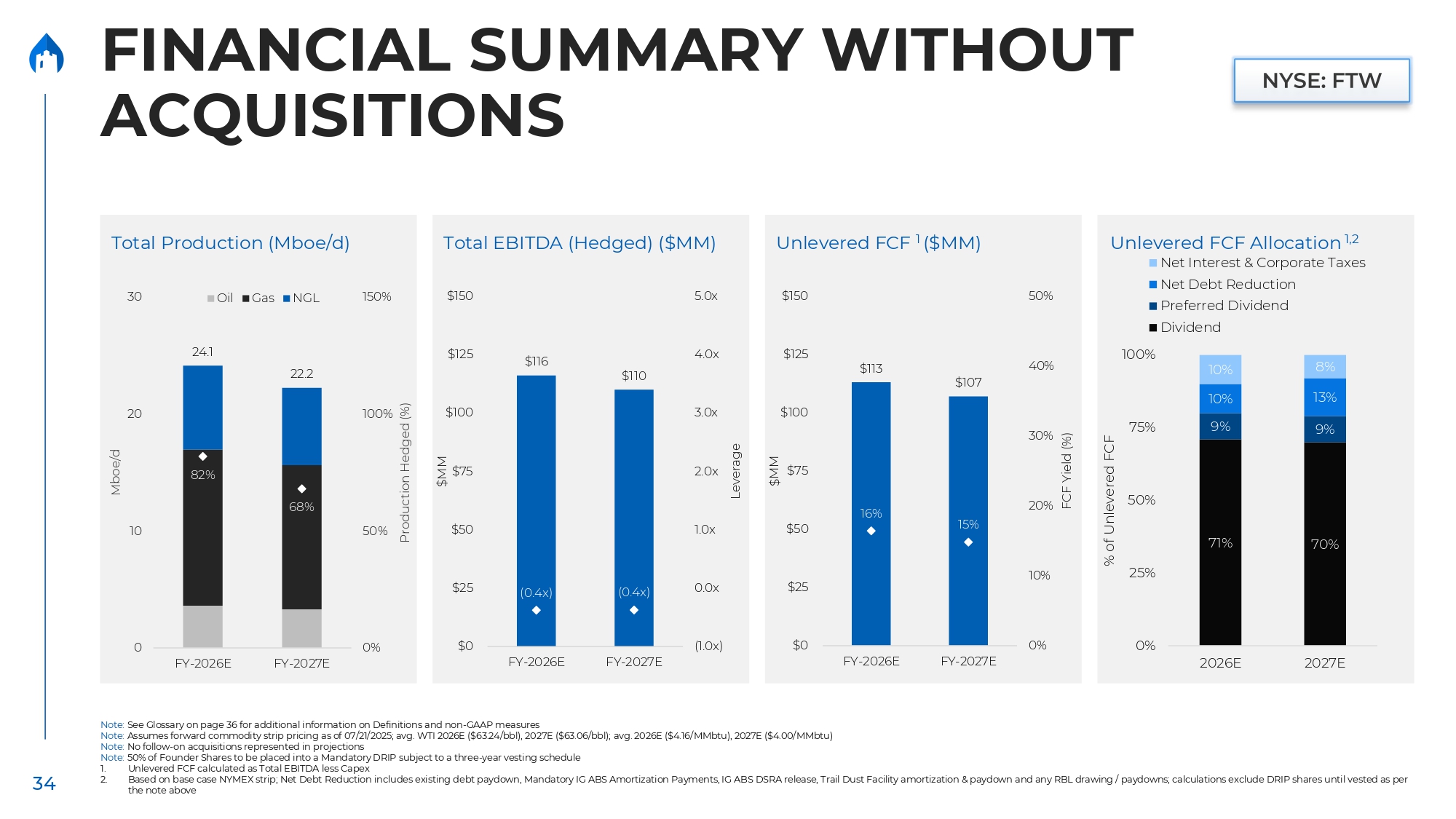

34 Total Production (Mboe/d) Total EBITDA (Hedged) ($MM) Unlevered FCF 1 ($MM) 24.1 22.2 82% 68% 0% 50% 100% 150% 0 10 20 30 FY - 2026E FY - 2027E Production Hedged (%) Mboe/d Oil Gas NGL $116 $110 (0.4x) (0.4x) (1.0x) 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x $0 $25 $50 $75 $100 $125 $150 FY - 2026E FY - 2027E Leverage $MM $113 $107 16% 15% 0% 10% 20% 30% 40% 50% $0 $25 $50 $75 $100 $125 $150 FY - 2026E FY - 2027E FCF Yield (%) $MM 0% 8% 10% 13% 10% 9% 9% 75% 50% 70% 71% 25% 100% 2026E 2027E % of Unlevered FCF Unlevered FCF Allocation 1,2 Net Interest & Corporate Taxes Net Debt Reduction Preferred Dividend Dividend FINANCIAL SUMMARY WITHOUT ACQUISITIONS Note: See Glossary on page 36 for additional information on Definitions and non - GAAP measures Note: Assumes forward commodity strip pricing as of 07/21/2025; avg. WTI 2026E ($63.24/bbl), 2027E ($63.06/bbl); avg. 2026E ($4.16/MMbtu), 2027E ($4.00/MMbtu) Note: No follow - on acquisitions represented in projections Note: 50% of Founder Shares to be placed into a Mandatory DRIP subject to a three - year vesting schedule 1. Unlevered FCF calculated as Total EBITDA less Capex 2. Based on base case NYMEX strip; Net Debt Reduction includes existing debt paydown, Mandatory IG ABS Amortization Payments, IG ABS DSRA release, Trail Dust Facility amortization & paydown and any RBL drawing / paydowns; calculations exclude DRIP shares until vested as per the note above

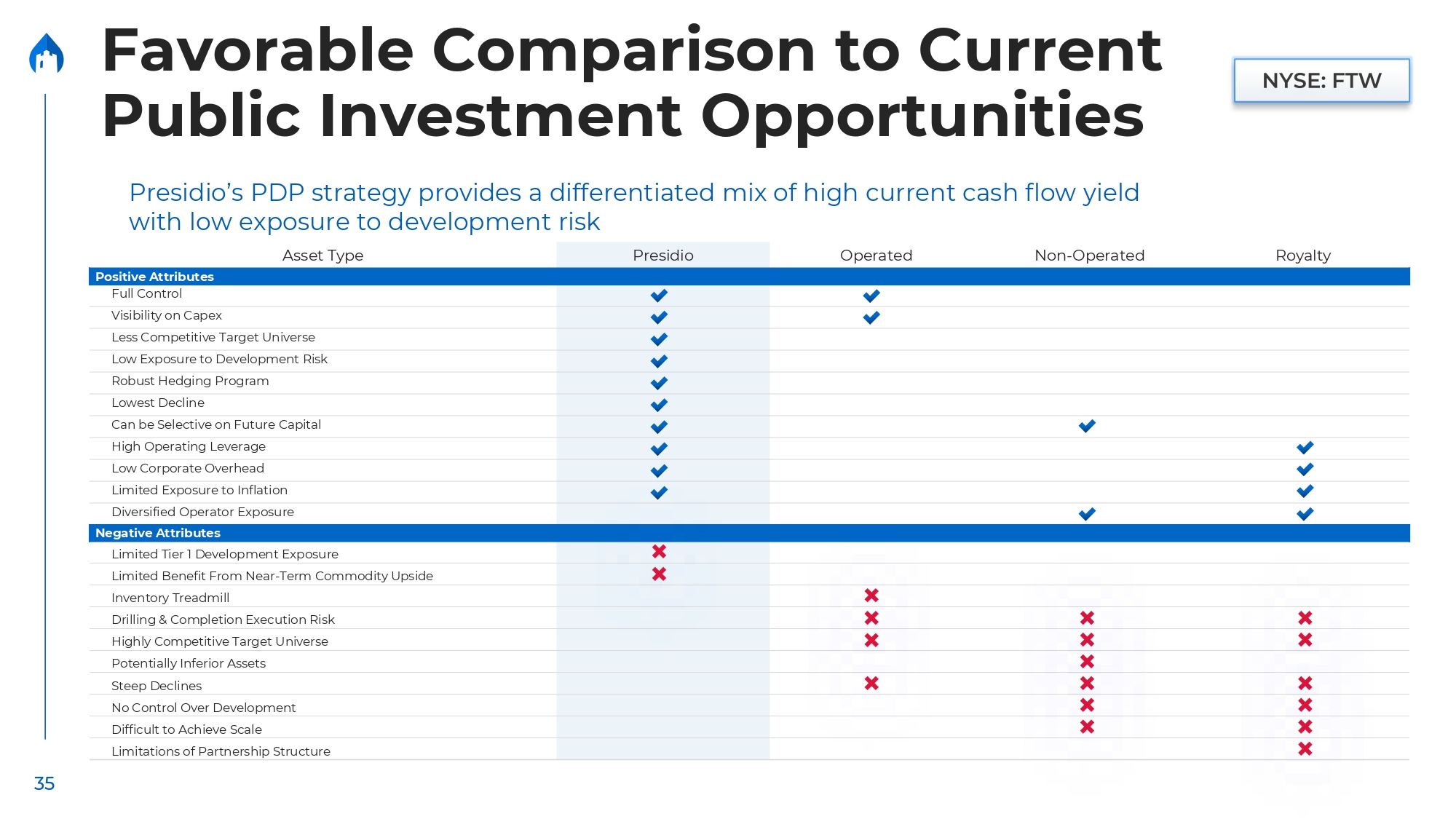

Favorable Comparison to Current Public Investment Opportunities Presidio’s PDP strategy provides a differentiated mix of high current cash flow yield with low exposure to development risk Asset Type Presidio Operated Non - Operated Royalty Positive Attributes Full Control Visibility on Capex Less Competitive Target Universe Low Exposure to Development Risk Robust Hedging Program Lowest Decline Can be Selective on Future Capital High Operating Leverage Low Corporate Overhead Limited Exposure to Inflation Diversified Operator Exposure Negative Attributes Limited Tier 1 Development Exposure Limited Benefit From Near - Term Commodity Upside Inventory Treadmill Drilling & Completion Execution Risk Highly Competitive Target Universe Potentially Inferior Assets Steep Declines No Control Over Development Difficult to Achieve Scale Limitations of Partnership Structure 35

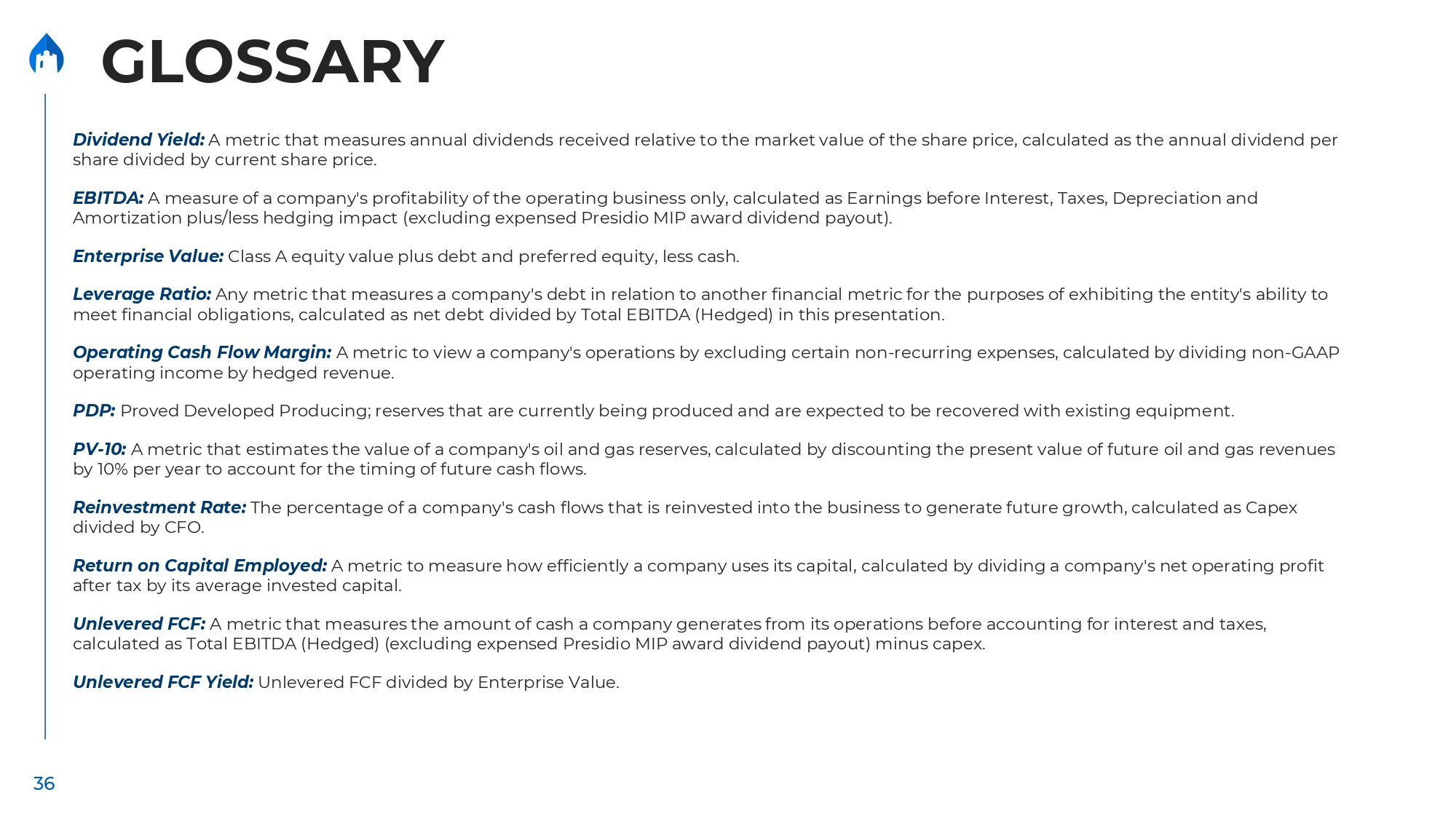

GLOSSARY 36 Dividend Yield: A metric that measures annual dividends received relative to the market value of the share price, calculated as the annual dividend per share divided by current share price. EBITDA: A measure of a company's profitability of the operating business only, calculated as Earnings before Interest, Taxes, Depreciation and Amortization plus/less hedging impact (excluding expensed Presidio MIP award dividend payout). Enterprise Value: Class A equity value plus debt and preferred equity, less cash. Leverage Ratio: Any metric that measures a company's debt in relation to another financial metric for the purposes of exhibiting the entity's ability to meet financial obligations, calculated as net debt divided by Total EBITDA (Hedged) in this presentation. Operating Cash Flow Margin: A metric to view a company's operations by excluding certain non - recurring expenses, calculated by dividing non - GAAP operating income by hedged revenue. PDP: Proved Developed Producing; reserves that are currently being produced and are expected to be recovered with existing equipment. PV - 10: A metric that estimates the value of a company's oil and gas reserves, calculated by discounting the present value of future oil and gas revenues by 10% per year to account for the timing of future cash flows. Reinvestment Rate: The percentage of a company's cash flows that is reinvested into the business to generate future growth, calculated as Capex divided by CFO. Return on Capital Employed: A metric to measure how efficiently a company uses its capital, calculated by dividing a company's net operating profit after tax by its average invested capital. Unlevered FCF: A metric that measures the amount of cash a company generates from its operations before accounting for interest and taxes, calculated as Total EBITDA (Hedged) (excluding expensed Presidio MIP award dividend payout) minus capex. Unlevered FCF Yield: Unlevered FCF divided by Enterprise Value.

Risk Related to Presidio's Business 37 → Presidio’s business depends on third - party transportation and processing facilities and other assets that are owned by third - parties. → The loss of a key member of Presidio’s management team, upon whose knowledge, relationships with industry participants, leadership and technical expertise the business relies on, could diminish Presidio’s ability to conduct operations and comply with certain covenants in Presidio’s debt instruments and harm Presidio’s ability to execute its business plan. → Oil, NGL and natural gas prices are volatile. Even though a significant portion of Presidio’s production is hedged, extended declines in such prices have adversely affected, and could in the future adversely affect, Presidio’s business, financial position, results of operations and cash flow. → Certain of Presidio's wells are currently shut - in, and in the future, Presidio may continue to shut - in some or all of its production wells depending on market conditions, storage or transportation constraints and contractual obligations. Any prolonged shut - in of its wells could result in the expiration, in whole or in part, of any related leases, which could adversely affect its reserves, business, financial condition and results of operations. → New technologies may cause the current operating methods of Presidio to become obsolete, and we may not be able to keep pace with technological developments in the oil and gas industry. → Conservation measures, technological advances and/or a negative shift in market perception towards the oil and gas industry could reduce the demand for oil, NGLs and natural gas. → Presidio’s estimated reserves are based on many assumptions that may prove to be inaccurate. Any material inaccuracies in these reserve estimates or underlying assumptions will materially affect the quantities and present value of Presidio’s reserves. → The present value of future net cash flows from Presidio’s proved reserves is not necessarily the same as the current market value of Presidio’s estimated proved reserves. → Extreme weather conditions could adversely affect Presidio’s ability to conduct operations in some of the areas where its properties are located. → Presidio has historically relied on third - party “farm - ins” and similar arrangements for the development of its proved undeveloped reserves. The development of Presidio’s proved undeveloped reserves may take longer and may require higher levels of capital expenditures than Presidio or such third - parties currently anticipate. Therefore, Presidio’s undeveloped reserves may not be ultimately developed or produced. → Presidio’s acquisition and divestiture strategy will subject Presidio to certain risks associated with the inherent uncertainty in evaluating properties for which Presidio has limited information. → Presidio may not be able to successfully integrate future acquisitions or realize all of the anticipated benefits from its future acquisitions, and Presidio’s future results will suffer if it does not effectively manage its expanded operations. → Presidio’s derivatives activities could adversely affect its cash flow, results of operations and financial condition. → The failure of Presidio’s hedge counterparties to meet their obligations may adversely affect Presidio’s financial results. → Presidio is not insured against all of the operating risks to which its business is exposed. → Financial projections by Presidio and information regarding prior performance may not prove to be reflective of actual future results. → The assumptions underlying our projections include our ability to consummate and realize the anticipated benefits from acquisitions in the future, which may never materialize. Such acquisitions, if any, may not be consummated on the terms and conditions underlying our assumptions, and results may, and are likely to, differ materially from such assumptions. → Presidio conducts business in a highly competitive industry. → Presidio depends on computer and telecommunications systems, and failures in those systems or cybersecurity threats, attacks and other disruptions could significantly disrupt its business operations. → A variety of stringent federal, state and local laws and regulations govern the environmental aspects of the oil and gas business, and noncompliance with these laws and regulations could subject Presidio to material administrative, civil or criminal penalties, injunctive relief or other liabilities. → Presidio is subject to compliance with environmental and occupational safety and health laws and regulations that may expose it to significant costs and liabilities. → Presidio's ability to retain and/or obtain necessary licenses and permits to operate the business may negatively impact its financial results. → Specific climate legislation and regulation regarding emissions of carbon dioxide, methane and other greenhouse gases have been, and in the future, may further develop or be enacted, which could adversely affect the oil and gas industry and demand for the oil, NGLs and gas produced from the properties. → The unavailability or high cost of drilling rigs, frac crews, equipment, supplies, personnel and oilfield services could adversely affect Presidio’s or third - party operators’ ability to execute their development plans within current budgets or on a timely basis. → Restrictions in Presidio’s existing and future debt agreements could limit Presidio’s growth and its ability to engage in certain activities. → Currently, Presidio’s producing properties are concentrated in the Anadarko Basin, making it vulnerable to risks associated with operating in a limited number of geographic areas. → Presidio may incur losses as a result of title or environmental defects in the properties in which it invests. Increased costs of capital could adversely affect Presidio’s business. → Presidio’s leverage and debt service obligations may adversely affect its financial condition, results of operations and business prospects. → Presidio’s ability to obtain financing on terms acceptable to it may be limited in the future by, among other things, increases in interest rates. → Oil and gas exploration and production companies are frequently subject to litigation claims from landowners, royalty owners and other interested parties, particularly during periods of declining commodity prices. → An increase in the differential between the benchmark prices of oil and natural gas and the wellhead price Presidio expects to receive for its future production could significantly reduce its cash flow and adversely affect its financial condition. → Oil and natural gas producers' operations are substantially dependent on the availability of water and the disposal of waste, including water and drilling fluids. Restrictions on the ability to obtain water or dispose of waste may impact Presidio's operations. → Increased scrutiny of Environmental, Social and Governance matters by investors in public companies could have an adverse effect on Presidio’s business, financial condition and results of operations and damage its reputation. → Legislation or regulatory initiatives intended to address the disposal of saltwater gathered from Presidio’s drilling activities could limit its ability to produce oil, NGLs and natural gas economically and have a material adverse effect on its business. → The securitizations of Presidio’s limited purpose, bankruptcy remote, wholly owned subsidiaries may expose Presidio to financing and other risks, and there can be no assurance that Presidio will be able to access the securitization market in the future, which may require it to seek more costly financing → While Presidio has not historically engaged in significant drilling activities, drilling for, and producing oil, NGLs and natural gas are high - risk activities with many uncertainties that could adversely affect Presidio’s financial condition or results of operations. → Presidio’s undeveloped leasehold acreage is subject to leases that will expire unless production is maintained or subsequent operations are commenced on units containing the acreage or the leases are extended. → Federal, state and local legislation or regulatory initiatives, as well as government reviews of such activities, could restrict Presidio’s operations, which could limit its ability to produce oil, NGLs and natural gas economically and have a material adverse effect on Presidio’s business.

Risk Related to Presidio's Business 38 → Presidio will be subject to business uncertainties and contractual restrictions while the Business Combination is pending. → EQV is, and Presidio would be after a Business Combination with EQV, an “emerging growth company” within the meaning of the Securities Act of 1933, and, if Presidio takes advantage of certain exemptions from disclosure requirements available to emerging growth companies, this could make the Presidio securities less attractive. → If there are substantial redemptions by shareholders of EQV, the trust account of EQV may be depleted prior to the Business Combination and thereby diminish the amount of working capital of the combined company. There would also be a lower float of our common shares outstanding after the Business Combination, which may cause further volatility in the price of our securities after the Business Combination and adversely impact our ability to secure financing following the closing of the Business Combination. → Shareholder litigation could prevent or delay the closing of the Business Combination or otherwise negatively impact our business, operating results and financial condition. → Our ability to successfully effect the Business Combination and to be successful thereafter will be dependent upon the efforts of certain key personnel. The loss of key personnel could negatively impact the operations and profitability of our post - combination business, and the combined company’s financial condition could suffer as a result. → Upon closing of the Business Combination, we expect to have a significant amount of cash and our management will have broad discretion over the use of that cash, subject to limitations imposed on us under the agreements governing our debt. We may use our cash in ways that shareholders may not approve. → Unanticipated changes in effective tax rates or adverse outcomes resulting from examination of our income or other tax returns could adversely affect our financial condition and results of operation. Going public through a merger rather than an underwritten offering presents risks to unaffiliated investors. → Subsequent to completion of the Business Combination, we may be required to take write - downs or write - offs, restructure our operations or take impairment or other charges, any of which could have a significant negative effect on our financial condition, results of operations and share price, which could cause you to lose some or all of your investment. → EQV and Presidio may not be able to obtain the required shareholder approvals to consummate the Business Combination. → EQV's initial shareholders, officers and directors may agree to vote in favor of the Business Combination, regardless how its public shareholders vote. → If, after EQV distributes the proceeds in the trust account to EQV’s public shareholders, EQV files a bankruptcy petition or an involuntary bankruptcy petition is filed against EQV that is not dismissed, a bankruptcy court may seek to recover such proceeds. → Presidio has incurred and will incur substantial costs in connection with the Business Combination, any private placement in connection therewith and related transactions, such as legal, accounting, consulting and financial advisory fees, which will be paid out of the proceeds of the Business Combination and the private placement, if any.