425: Prospectuses and communications, business combinations

Published on September 29, 2025

Filed by Prometheus PubCo Inc.

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Prometheus PubCo Inc.

Commission File No.: 333-290090

Date: September 25, 2025

The following article was published by S&P Global Commodity Insights on September 25, 2025.

INTERVIEW: Producer Presidio to take its PDP ‘asset manager’ model public

Author: Jeremy Beaman

IPO to follow tie-up with EQV Ventures Acquisition

Current operations span the Anadarko Basin

Company now weighted about 50% dry gas

Presidio Petroleum wants to give investors a chance to buy into the market’s first “real 100% true" proved developed producing oil and natural gas player, co-CEO Will Ulrich told Platts in a recent interview, as it works toward an initial public offering by year's end.

For the most part, those in the market for exposure to upstream oil and natural gas have to choose from a slate of exploration and production companies built around drilling and completing new wells. As those wells age, decline and become less economic, E&Ps look to offload some of those assets.

Since its founding in 2017, Presidio has been seeking out those aging “PDP” wells, seeing in them an opportunity to operate them more cheaply and to generate significant cash, Ulrich, a co-founder of Fort Worth, Texas-based Presidio said.

“We decided early on that the economics of drilling were not as good on a full-cycle development cost as people had advertised,” he said. “And so we should stay away from that instead focus on the acquisition of wells that we felt we could operate better, increase margins, increase cash flow, invest in the production through workovers over time when commodity prices were good.”

PDP focus

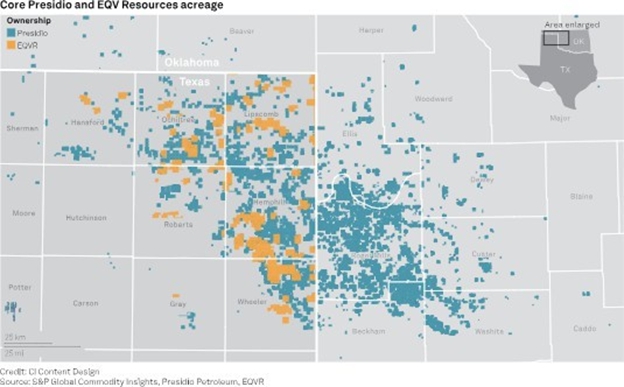

Presidio currently operates more than 2,000 PDP wells in the Anadarko Basin, with assets concentrated in the Texas Panhandle and Oklahoma.

As announced in early August, the company agreed to merge with a special purpose acquisition company, EQV Ventures Acquisition, whose sponsor EQV Group has more than 1,800 PDP wells under management.

Through the combination, the pro forma Presidio Production Company is valued at approximately $660 million and targeting a public listing by the end of the year. The combined company would absorb and operate some EQV wells alongside Presidio’s incumbent assets, and total operated wells would rise to more than 2,300.

Presidio also has undeveloped acreage but would look to partner with outside operators and carry interest in any new wells rather than expend its own capital to drill, Ulrich said.

“Even other companies that are public that are positioned as more kind of cash flow, PDP yield co-type players, they're still reinvesting 20%, 30% of their free cash flow into additional development, whereas we are zero,” Ulrich said.

To grow, Presidio will seek out additional assets PDP assets and has modeled spending $200 million, $300 million and $400 million consecutively on transactions across its first three years as a public operator.

Acquisition opportunities across the Midcontinent are valued at about $725 million, with another $450 million across the Haynesville Shale and $200 million in the Barnett Shale, according to the company’s investor presentation.

“There is a, I think, a supply-demand imbalance for this type of asset, between how many buyers are interested and how many sellers, or how much asset that exists,” Ulrich said. “And broadly, if you think about the industry, we're like -- we're an asset manager, and so we're not -- we don't participate in the growth portion of the value chain.”

Philosophy and strategy

Most public upstream producers are ever concerned with adding drilling opportunities as depth of undeveloped locations is a big determinant of value.

“To study Presidio and make an investment decision, you don't need to underwrite … acreage, inventory, years of inventory at different rates of drilling and consumption, et cetera,” Ulrich said. “It's really a cash flow business that's offering an attractive yield with the ability to grow that yield through accretive acquisitions.”

2

As shale continues to mature, operators’ businesses will likely have to look more like Presidio’s does today, Ulrich also said.

“As more and more wells are drilled up, more and more locations are consumed, more and more -- and I think the industry is already shifting this way – more and more of the industry's focus is going to have to be just on asset management as opposed to growth,” he said.

Presidio is undertaking its IPO effort at a time defined by low forward crude oil prices and a natural gas market that, though dealing with soft prices of late, is widely expected to grow hotter in 2026 owing to rising gas demand.

Presidio seeks cash flow stability by hedging a large majority of its production, with 78% of its volumes hedged out through 2027 and additional protection already in place at lower levels through 2030, Ulrich said.

“When commodity prices are low, we have this great hedge protection that's paying us and, in fact, we kind of get the increased benefit of as commodity prices drop, our expenses in the field tend to drop as well," Ulrich said.

As prices rise, the company can work through a backlog of well workovers that weren't economic in a lower price environment.

Standalone Presidio is expected to produce 22,500 boe/d this year, about half of which is dry gas, 35% NGLs and the remainder crude oil. The pro forma company would produce an estimated 25,700 boe/d.

“As we look at where we think maybe we can achieve the best cost of capital, I think there's probably some advantages to being a gassier player,” Ulrich said. “Though, that said, I think there are some structural kind of mismatches in the supply-demand and what prices are reflecting on the oil side, which could just be attractive from a fundamental investing standpoint.”

3

Forward-Looking Statements

This article includes “forward-looking statements.” These include any of EQV Ventures Acquisition Corp. (“EQV”), Prometheus PubCo Inc. (“Presidio”) or Presidio Investment Holdings, LLC (“PIH”) or their management teams’ expectations, hopes, beliefs, intentions or strategies regarding the future. Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “potential,” “budget,” “may,” “will,” “could,” “should,” “continue” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding Presidio’s, PIH’s and EQV’s expectations with respect to future performance, the capitalization of EQV or Presidio after giving effect to the proposed business combination and expectations with respect to the future performance and the success of Presidio following the consummation of the proposed business combination. These statements are based on various assumptions, whether or not identified in this article, and on the current expectations of Presidio’s, PIH’s and EQV’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied upon by any investors as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of Presidio, PIH and EQV. These forward-looking statements are subject to a number of risks and uncertainties, including changes in business, market, financial, political and legal conditions; benefits from hedges and expected production; the inability of the parties to successfully or timely consummate the proposed business combination, including the risk that any regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect Presidio or the expected benefits of the proposed business combination or that the approval of the shareholders of EQV is not obtained; failure to realize the anticipated benefits of the proposed business combination, which may be affected by, among other things, competition, the ability of Presidio to grow and manage growth profitably, maintain key relationships and retain its management and key employees; risks related to the uncertainty of the projected financial information with respect to PIH or Presidio; risks related to PIH’s current growth strategy; the occurrence of any event, change or other circumstances that could give rise to the termination of any definitive agreements with respect to the proposed business combination; the outcome of any legal proceedings that may be instituted against any of the parties to the potential business combination following its announcement and any definitive agreements with respect thereto; changes to the proposed structure of the proposed business combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the proposed business combination; risks that PIH or Presidio may not achieve their expectations; the ability to meet stock exchange listing standards following the proposed business combination; the risk that the proposed business combination disrupts the current plans and operations of PIH; costs related to the potential business combination; changes in laws and regulations; risks related to the domestication of EQV as a Delaware corporation; risks related to Presidio’s ability to pay expected dividends; the extent of participation in rollover agreements; the amount of redemption requests made by EQV’s public equity holders; and the ability of EQV or Presidio to issue equity or equity-linked securities or issue debt securities or enter into debt financing arrangements in connection with the proposed business combination or in the future. Additional information concerning these and other factors that may impact such forward-looking statements can be found in filings and potential filings by PIH, EQV or Presidio resulting from the proposed business combination with the SEC, including under the heading “Risk Factors” in the registration statement on Form S-4 (the “Registration Statement”) originally filed with the U.S. Securities and Exchange Commission (“SEC”) by Presidio and PIH on September 8, 2025. If any of these risks materialize or any assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that none of Presidio, PIH nor EQV presently know or that Presidio, PIH or EQV currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by investors as a guarantee, an assurance, a prediction or a definitive statement of fact or probability.

In addition, forward-looking statements reflect Presidio’s, PIH’s and EQV’s expectations, plans or forecasts of future events and views as of the date they are made. Presidio, PIH and EQV anticipate that subsequent events and developments will cause Presidio’s, PIH’s and EQV’s assessments to change. However, while Presidio, PIH and EQV may elect to update these forward-looking statements at some point in the future, Presidio, PIH and EQV specifically disclaim any obligation to do so, except as required by law. These forward-looking statements should not be relied upon as representing Presidio’s, PIH’s or EQV’s assessments as of any date subsequent to the date they are made. Accordingly, undue reliance should not be placed upon the forward-looking statements. None of Presidio, PIH, EQV, or any of their respective affiliates have any obligation to update these forward-looking statements other than as required by law. In addition, this article contains certain information about the historical performance of PIH. You should not view information related to the past performance of PIH as indicative of future results. Certain information set forth in this article includes estimates and targets and involves significant elements of subjective judgment and analysis. No representations are made as to the accuracy of such estimates or targets or that all assumptions relating to such estimates or targets have been considered or stated or that such estimates or targets will be realized.

4

Additional Information and Where to Find It

In connection with the proposed business combination, Presidio and PIH filed the Registration Statement with the SEC, which includes a prospectus with respect to Presidio’s securities to be issued in connection with the proposed business combination and a preliminary proxy statement with respect to the shareholder meeting of EQV to vote on the proposed business combination. EQV, Presidio and PIH also plan to file other documents and relevant materials with the SEC regarding the proposed business combination. The Registration Statement has not yet been declared effective by the SEC. After the Registration Statement is declared effective by the SEC, the definitive proxy statement/prospectus will be mailed to the shareholders of EQV as of the record date to be established for voting on the proposed business combination. SECURITY HOLDERS OF EQV AND OTHER INTERESTED PARTIES ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS AND RELEVANT MATERIALS RELATING TO THE PROPOSED BUSINESS COMBINATION THAT WILL BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BEFORE MAKING ANY VOTING DECISION WITH RESPECT TO THE PROPOSED BUSINESS COMBINATION BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND THE PARTIES TO THE PROPOSED BUSINESS COMBINATION. Shareholders are able to obtain free copies of the proxy statement/prospectus and other documents containing important information about Presidio, PIH, and EQV once such documents are filed with the SEC through the website maintained by the SEC at http://www.sec.gov. In addition, the documents filed by EQV may be obtained free of charge from EQV at www.eqvventures.com. Alternatively, these documents, when available, can be obtained free of charge from EQV or Presidio upon written request to EQV Ventures Acquisition Corp., 1090 Center Drive, Park City, Utah, 84098, Attn: Secretary, or by calling (405) 870-3781. The information contained on, or that may be accessed through the websites referenced in this article is not incorporated by reference into, and is not a part of, this article.

Participants in the Solicitation

EQV, PIH, Presidio and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of EQV in connection with EQV’s shareholder meeting. Security holders may obtain more detailed information regarding the names, affiliations and interests of certain of EQV’s executive officers and directors in the solicitation by reading EQV’s annual report on Form 10-K, filed with the SEC on March 31, 2025, the definitive proxy statement/prospectus, which will become available after the Registration Statement has been declared effective by the SEC, and other relevant materials filed with the SEC in connection with the proposed business combination when they become available. Information concerning the interests of EQV’s participants in the solicitation, which may, in some cases, be different from those of EQV’s shareholders generally, will be set forth in the preliminary proxy statement/prospectus included in the Registration Statement.

No Offer or Solicitation

This article shall not constitute a solicitation of any proxy, vote, consent or approval in any jurisdiction in connection with the proposed business combination and shall not constitute an offer to sell or a solicitation of an offer to buy the securities of EQV, PIH or Presidio, nor shall there be any sale of any such securities in any state or jurisdiction in which such offer, solicitation, or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended. This article is restricted by law; it is not intended for distribution to, or use by any person in, any jurisdiction in where such distribution or use would be contrary to local law or regulation.

5